I did a presentation on this long ago (The original presentation can be downloaded from here: Uberization of Money Transfer: 12 Questions every small and medium, independent money transfer operator should ask themselves). For months I’ve been thinking of doing an updated version of the presentation into an article, so here it is. It is a long article, but if you’re from the industry, you will then most likely understand what I have stated and appreciate the solutions.

The world of money transfer is getting competitive by the minute. Not only is the landscape filled with multiple players, the time, material and monetary resources required to keep abreast of things, is taxing enough for many.

The Problems

There are 1000s of small and medium, independent money transfer businesses around the world. Most of them are struggling and the ever present threat of shuttering down is a very serious issue they face.

Here are just some of the issues that small money transfer businesses have to deal with:

- Costs of maintaining licenses

- Money required to expand sales & marketing efforts

- Money and human resources required to invest and keep up with technology

- Investing in better customer support

- Ever increasing compliance costs

- Online presence

- Maintaining access to banking

- Ever present threat of being de-risked by your bank

- License coverage in other parts of the country and world

- Limited payout network

- Not being able to expand the type of customers (B2B, B2C, B2B2C payments, for example)

- Bringing value-added services like bill payment, mobile top-ups

- Limited pre-funding money

- Managing all this with the daily fire-fighting that is going on

- How to compete against the big-guns like Transferwise, Xoom, Western Union, MoneyGram, etc.

- Technical integration with other players, payment networks and payment systems

- Training

- Brand management, etc.

If you’re from the industry, then you know, just by reading the above-mentioned list would make anyone’s blood pressure go low. Depression is a real threat (and I’m not joking here).

Money transmitters and other MSBs experience real fear of de-risking while banks and credit unions experience what could be imagined fear of banking MSBs.

Credit: From: Use Your BSA Risk Assessment to Build Banking Relationships by Mark Stetler – Co-founder and CEO RegSmart as appearing in David Landsman Consulting – Daily Digest Newsletter – 26 March, 2019

Link: https://www.amlservices.us/

The Analogy

I always give this example, so think about the following. If I were to ask you how many banks in the United States, the approximate answer is about 8,000 (give or take). This includes all sorts and types. Large, Small, Community Banks, Credit Unions, etc.

How many of them are Tier I banks? with say assets over $500 Billion. The answer might be 10 or 20, or even 50, but let’s round it up to 100. So we have 100 Tier I banks in the US. This leaves us with 7,900 Tier II and Tier III banks.

Second question: How many Tier II banks in the US? Tier II would represent assets between $10 Billion to less than $500 Billion. The answer this time around might say 50 or 75 banks. Let’s again round this off to say 200 Tier II banks. So now we have 7,700 Tier III banks left.

Tier III banks are banks with assets size under $10 Billion. This represents the majority of small and medium banks in the United States. From one-branch, one-city banks to a few dozen branches and a few states.

Now that we have set this viewpoint, let me ask you the following questions:

- Who provides the software and services for CORE Banking to the Tier I Banks? Answer: they themselves. In most of the cases, these large banks use their own bespoke software, developed and refined over the years. Some of them use vendors like Temenos of Misys, etc.

- Who provides the software for Tier II and Tier III? Answer: The commercial vendors like Jack Henry & Associates, FIS Global,

FiServ , Temenos, Misys (now calledFinastra ), etc.

For most of the 7,700 banks, the technology part is handled by the Big 3 cartel. Yes, it is a cartel, you can listen to this podcast to learn more about how the CORE Banking Cartel in the United States operates:

(Around The Coin – Episode 159: The Oligopoly in American Banking that no one talks about).

Who Serves the Money Transfer Businesses?

So, coming to the Money Transfer Businesses, how many of them are there around the world? My guess let say 50 money transfer companies per country (leveling out), and about 200 countries and territories world over, would yield approximately, 10,000 money transfer operators.

Again, how many are Tier I Money Transfer Operators (MTOs)? Those that are licensed in multiple countries, that operate and channel more than $10 Billion per year? Probably 10? 20? 30? players. Round it off to 100. So, 100 MTOs.

How many of them are Tier II Money Transfer Operators? Those licensed in single &/or multiple geographies, but perhaps operate between $1 Billion to less than $10 Billion? Again, the same number about 100 or so Tier II. Let’s quadruple it to 400 Tier II MTOs.

So we then have about 9,500 Tier III MTOs. Licensed in a single market. In some case licensed in multiple locations. Processing well under $1 Billion per year. In most cases, limited geography, limited to a few stores (if at all) and serving a very limited corridor network.

Here is the multi-million dollar question: Who are the Jack Henrys or FIS Global or FiServs to the 9,500 Money Transfer Operators around the globe.

The answer: No one.

That’s right. As a Tier III Money Transfer Operator, you have to fend for yourself. There is no one on your team. You have to walk the journey alone, and fight all the battles, alone. Obstacles plenty, help, practically none.

Who’s taking care of you? No one …yet!

This is the problem that obsessed me for years. Truth be told, it is one of the problems that has obsessed me. Other is real-time (read: instant), low-value, affordable, cross-border payments. Anyhow, I digress. So before I give the solution (or you could just scroll down), let me amplify the problem.

Q1: How close or distant are you from your competition?

Are you at par with your competition? Are you close? If we talk about established players like Western Union or MoneyGram, how are you positioned against them? What about the de novo players like Transferwise, Xoom, WorldFirst, etc.? If you are a Tier III player, it is no secret, you envy the established players. You not only envy the de novo players but secretly despise them for pushing the prices lower.

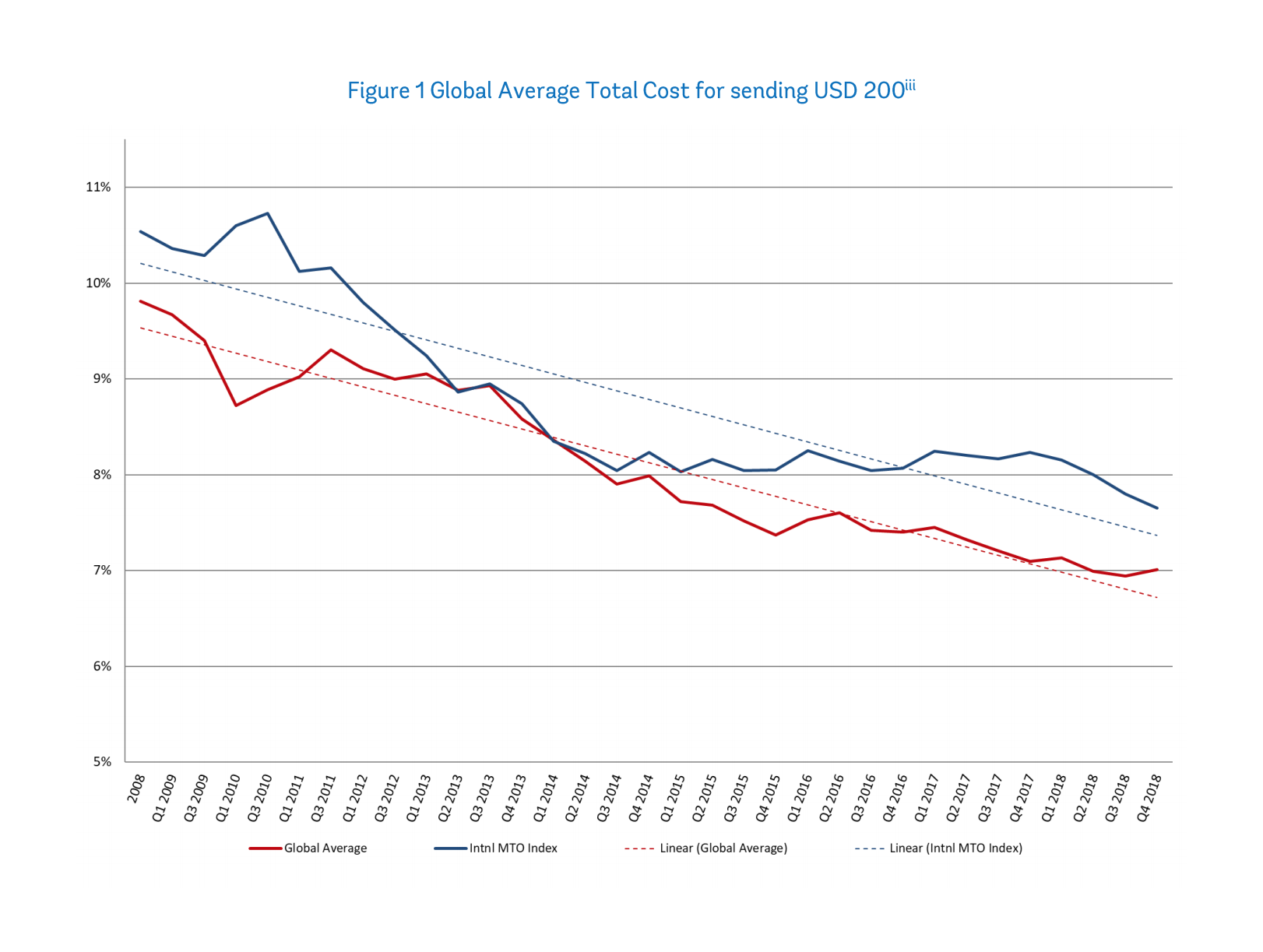

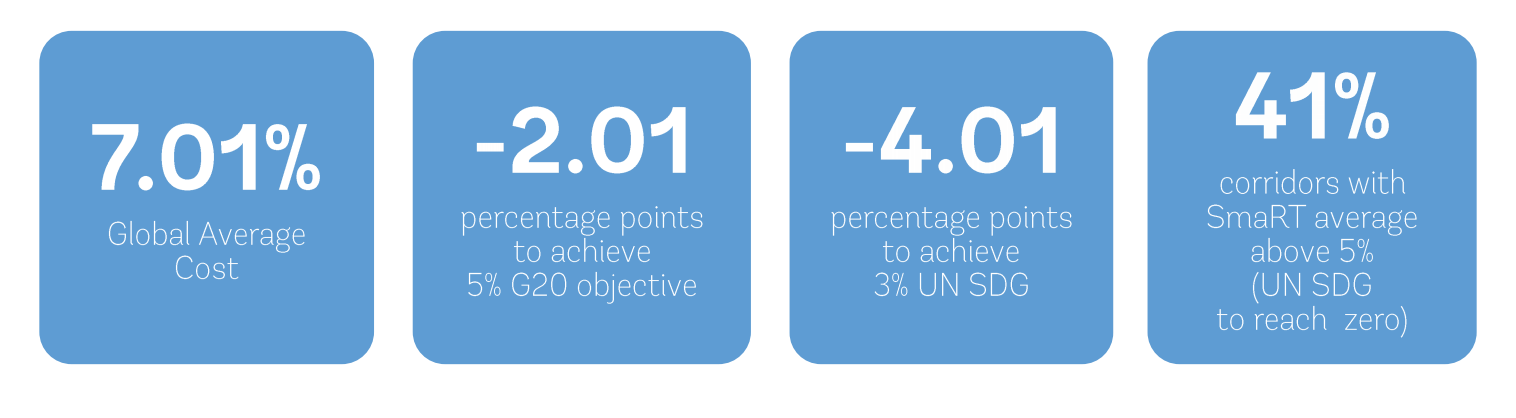

Let’s just come out with it: You hate them! Deep down inside, you blame them for your diminishing profits. The truth is, you are too scared to admit the reality yourself. That with competition, prices are falling. Eventually, they will fall way below the threshold you have marked, in order to survive. This is how the industry works. New entrants bring downward pressure. This is no hidden secret. In fact, you already know about this. Everyone knows about this. The World Bank Group publishes a report literally every quarter for the last 10+ years, highlighting this: Cost of sending money is going down.

The World Bank has set a goal to bring the average cost of remittances down to 3% (300 basis points) by the year 2030. Companies like Ripple have said publicly, that if they are not able to bring the price of cross-border money transfer down to 30 basis points (0.3%) – they (Ripple) would have failed in their mission. (See this fireside chat, I had with Brad Garlinghouse, CEO of Ripple in 2018 at Money 20/20 Asia in Singapore)

So the truth of the matter is. You know this has been happening, from Day 1. But now, the speed at which this decline is happening has accelerated, which bring the doomsday scenario a lot closer.

In another 11 years (by 2030), the price of sending money (on average, worldwide) will be 3%. This means in many of the competitive corridors (US-India, UAE-Pakistan, Saudi Arabia-Bangladesh, Hong Kong-Philippines, US-Mexico) the price of sending money will be a few 10s in basis points. Definitely under 1% and most likely under 0.5%.

How will you survive then? Or will you even be in business? Will you still blame the incumbents and de novo players?

Q2: How strong and prominent is your online social media presence?

The world is moving online. If you disagree. Stop reading this and go back to what you were doing.

Let me give my own internal study example. Let’s take a market like the United States and pick any particular segment, say, Latin America. This is how the figures for US-LatAm market looked like in 2017:

- 84% of all money transfers were at an off-line, physical location (non-banks)

- 6% of all money transfers were online, by NBFIs (Non-Banking Financial Institutions), i.e. your MSBs / MTOs / MSOs

- 10% of all money transfers were done by banks (be it online, offline, at a branch location, over the phone, internet banking, etc.)

In 2010 the online figure was less than 2%. What do you think the online figure will be in 2020? by 2025? and by 2030?

Here are my guesses

- By 2020: it will be at about 8%

- By 2025: 15%, and

- By 2030: 40% and above

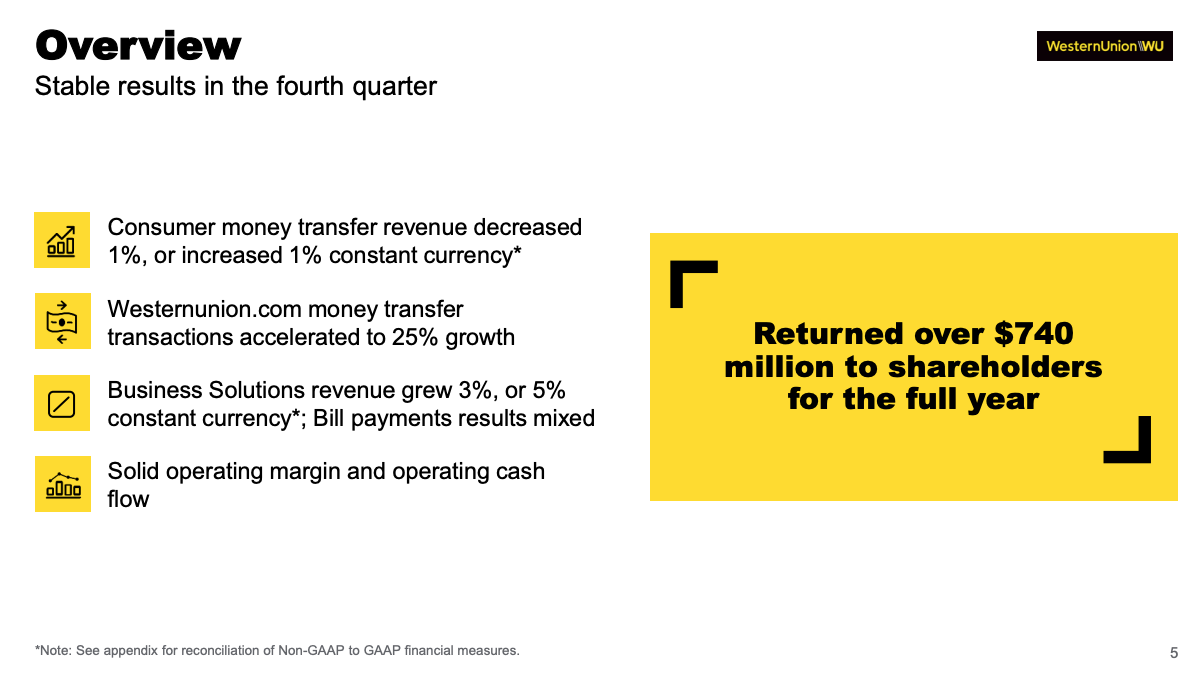

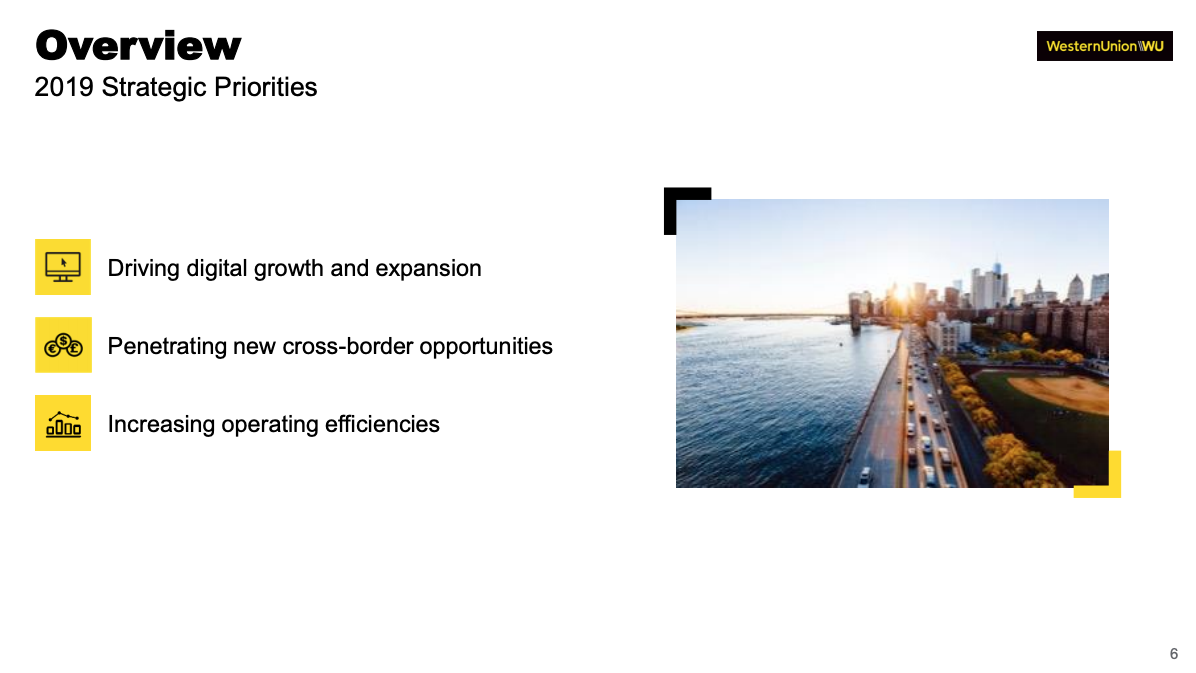

Western Union is investing heavily in Western Union online and realizing that the online platform is the next-generation platform to conduct business on, in light of the diminishing physical agent network. WU recognizes this by a story someone once told me (I cannot verify the claim, so if anyone can, please let me know). The story goes that in every Western Union Board meeting, they bring a large printed

Look at the following two screens from the earnings call presentation:

Notice that Westernunion.com

Driving digital growth and expansion is their #1 priority for 2019. In this day and age, where banks are derisking themselves and malls are closing down, where the cost of compliance is going high, where cash is frowned upon, agents are struggling and demanding more compensation for declining commissions, where do you think all this is going?

WU knows the end game.

That may be in 10 years, the size of the physical agents market will perhaps be reduced by 50% Where do you think all that reduced traffic will go to send money? They will go online! WU will eventually cannibalize their Agent network for the online network. This will not be offline vs online. It will be a hybrid solution for some time to come and the online will eventually win. You can read the Western Union Fourth Quarter 2018 Report (PDF) here.

By merely having a Twitter account or Facebook page, one does not acquire customers. Most of the Tier III Money Transfer Businesses don’t even have

How many customers are you signing up that came through social media? If the answer is none, you’re dead! You just don’t know it. You cannot just invest in social media and expect everything to be smooth tomorrow. It takes months and months (if not years) of hard work before your online brand reputation even starts to take shape. A classic case of a job well done, that literally took years to establish is XpressMoney. Look at their Twitter feed and it is one of the best ones I follow (and I follow and monitor a lot of feeds). @XpressMoney makes their feed a right mix of work, family, fun and knowledge balance. A lot many money transfer business players in the space have taken their social media cue from @XpressMoney.

Q3: How much money are you spending on online advertising and affiliate programs to solicit clients?

Sign-up for an affiliate of Transferwise and you can earn serious money up to $ 50 for every user you refer to them. TW’s affiliate program has 1,000s of participants, churning our content on the internet in the hopes of catching new clients. Transferwise is okay with paying out $50 commission to you, for acquiring a new customer. It is estimated that the cost of acquiring a new customer for Western Union or MoneyGram is less than $15 per customer.

For others, they are not so lucky. Economies of scale don’t benefit them. They have to fight and up the game to win customers. It is estimated by various analysts that the actual cost of acquisition of a new client by Transferwise is perhaps as high as $75 per customer (if you include costs like advertising, etc.)

Tier III providers have it worse. They are already cash strapped. Can you afford to pay an affiliate $50 per every new customer acquired? Even if you did. How much will you earn per customer? $10? $15? $25. How many months before the customer becomes profitable for you? By merely having a Twitter account or Facebook page, one does not acquire customers. Most of the Tier III Money Transfer Businesses don’t even have

You have to have a social media strategy and then spend money to execute that strategy. One huge problem with small Tier III providers is that to save money, they will attempt to do everything themselves. They will embark and try to launch their own social media presence and suck at it. They will spend money on ads without knowing how online ads work and blow large sums of money and not get any results. All this will lead to more frustration and throwing in the towel.

What happens after this? The natural knee-jerk reaction is to blame everyone else, but yourself for the failures. You need help, but you can’t afford it.

Q4: How much money are you spending on your front-end and back-end technology?

Relationship building is core differentiator as to why people do business with you (amongst other factors), but a lot of that relies on technology. Technology is the core internal differentiator. Without a solid technology stack, most Money Transfer Operators struggle to make things work. Ask anyone if their IT team is good, and the reply I always hear is “My IT team is the best”. This could not be further from the truth. Whilst, IT teams are generally good. They are not the best. Tier III simply cannot afford to hire nor retain the best of IT.

The economics just do not work out.

Keeping pace with the technological advances literally requires a small team (read: army). Today you need information architects, API specialists, database specialists, cyber/network security specialists, full-stack developers, UI/UX specialists, and mobile application programmers. Small money transfer operators sometimes live paycheck to

Even with the various vendors out there in the market, who purportedly are looking after your interests (they are not), you don’t save much. Every feature request, every feature unlocking, every bit of report generation or backup exercises, etc. are added billable hours or an increase in the monthly subscription.

While Software-as-a-Service (SaaS) providers have reduced the burden of IT a lot, they don’t necessarily solve the operational quagmire you are in. Death of your business is assured if you do not invest in IT/Technology. Compliance requires more automation and controls. So do your regulators. So do your banking and payment network partners. And, more importantly, so do your customers.

With very limited resources, it is no small wonder that almost every small Money Transfer Operator I speak to are struggling on this front and rarely do they admit to others.

As friends, I happen to get this candid admission out of them.

Q5: How many beneficiary countries do you have access to whilst still being competitive?

Most Money Transfer Operators who are classified as Tier III, operate and serve in very specific ethnicity and geography. Some do a few more as they go along, but for a large swath, Tier III MTOs know their niche. For years, they have been operating/serving their focused market. As more de novo players have entered, they now slowly see their corridors being threatened. In addition to this, Tier III operators also lack the time, resources and capital to expand on to other markets. I’ve personally known providers who say are active in Bangladesh and Pakistan and when I ask them why they don’t expand to India, Nepal and Sri Lanka, they always claim they don’t have the bandwidth for it.

Same with Tier III providers who service Tanzania and Kenya, why don’t they branch out to Ghana, Rwanda, and Ghana. Same variation of the story always. Don’t have the capital or the technology stack to expand out. It is not as if the Tier III providers are oblivious about aggregators, but they keep citing and I believe them, that in most of the time, aggregators are not able to offer a competitive rate for them to do business.

What most Tier III providers don’t realize is that the fewer the corridors, the more risk their business is prone to. It is the proverbial equivalent of putting all your eggs in one basket. Should a corridor go down (for whatever reason), it will have a significant impact on business. Hence, expanding and spreading your risk across multiple markets is always a better choice.

Expansion is easy. A competitively priced expansion is not, and, herein lies the problem. How do you expand to other corridors with a price point that is competitive with what the customers are paying right now for

Q6: Are you considering expanding your licenses to other states & territories?

Applying for licensing is expensive when you’re small. Once you have enough traction going, and your market research supports expansion, then, by all means, do it. Reality is most Tier III Money Service Operators (MSOs) sit on the fence when it comes to expansion. Getting additional licensing means committing more human, technological and capital resources to achieve that goal. An option that most Tier III Money Transfer Businesses just can’t exercise.

Even if they do get licensed then the corollary of marketing and sales needs to be addressed. Soon enough you realize this is a chicken and the egg situation on so many fronts.

You should take a cue from the world of travel agents, or freight forwarders or even the real estate industry. They get access to each other’s markets by leveraging the power of an association. A travel agent joins a hotel or an airline network that enables wider market access. Freight forwarders discovered this years back and that is how freight moves around the world today. The real-estate industry hinges its success behind the Multiple Listing Service (or MLS) which allows a home buyer or seller to gain access to properties that otherwise were not in their real-estate agents geographic or marketing reach.

Individual licensing expansion can be a huge capital burden (not to mention, an operating resources burden as well). However, this load can be lightened by leverage or pooling in your license with those of others. You cannot have your cake and eat it too. The MLS success hinged on this. Shared sales are better than no sales.

Q7: If your geographic reached expanded by getting licenses in other states, how many more clients do you think you would be able to get?

It is always great to daydream… Here are some great questions to daydream over:

- What if we had a New York license?

- What if we had a Texas license?

- What if we had money transmitter licenses for the New England states?

- What would happen if tomorrow we suddenly had access to the California market?

- What if we could get a Pan-European license to pick up customers from all over Europe?

These are questions you should be asking yourself all the time. Once you’ve asked the questions, the next goal should be to understand the market itself.

- How big is the market?

- What sort of opportunity exists?

- How many players dominate?

- Which corridors present an opportunity that we could tackle remotely?

- What are our existing customers saying about these markets?

- What has our marketing research and surveys told us?

- Do economies of scale kick in, should we expand to these additional markets?

- What sort of operational and back-office burden does it create?

- What do the income estimates say?

- How profitable will the routes be?

- What sort of market can we capture and how?

- Over what period?

- What marketing budget would be required?

- How much more additional working capital would be required?

Many money transfer operators would like to expand, and believe me, expansion is easy and doable, but you have to do your own market research and study on the feasibility. The merchantability of your expansion plans is something only you know best. The sooner you start devoting time towards the completion of these go-to-market studies, the sooner you would be ready (not to mention confident) in executing such opportunities and actually expanding.

Do it.

Note

Remember the 5 P’s: Prior Planning Prevents Poor P

If you are serious about understanding how to go about this, I wrote a slightly tangential article called Architecting a mobile wallet that customers want. You can read on how to map the user journey and conduct surveys, etc. If nothing, it will perhaps give you some form of semblance on how to start thinking about market research & survey.

Q8: Is your ability to expand restricted by the lack of capital?

Access to capital, i.e. money is a core tenant for any business. Money Transfer Businesses are no exception. Everyone seems to be stuck on a line of thinking that they need to come up with money in order to expand. Traditional thinking would say yes, but if you can recalibrate your mind to think differently, there are many innovative ways to expand, without the need

Your license is your leverage. You existing markets, customers, your domain knowledge alone are your leverages.

What good would a blog post be without a song about money! This is how sadly every independent Money Service Operator that I know of is thinking (a great song called “Gotta Get My Hands on Some Money” by Fatback).

In all seriousness, if this is what you are obsessed over, it is a good thing, but direct the obsession towards earning that money with what you have right now, rather than getting money (magically) from somewhere. This is what sales and growth hacking is all about. Finding innovative methods to pump the numbers with minimal or no investment whatsoever.

There is a reason I used the word recalibrate your mind. Let go of the traditional approaches and think How, with what you have, can you trade?

Capital is not the limiting factor here.

Your ability to think-outside-the-box-and-do-deals is.

Q9: How are you adding new products & services?

Many small and medium MTOs are for years doing the same thing day-in, day-out. Remittance. People sending money to People. Mostly family remittances. Nothing changes over the years. The MSOs become so complacent and ingrained in what they are offering, that I personally think, they are blindsided by the options around them. You need not scale horizontally. You need to look vertically. What are the value-added payments you can offer to your existing clients?

The above is an example diagram of what a typical value-added payment stack looks like in P2P payments. This stack is not etched in stone, so feel free to modify it as per your availability. The goal is to look at payments in a different light and understand what additions, improvements, enhancements can be done.

In addition to the above stack, there are also other payment types you may need to look at. Business-tConsumer payments, (typically denoted as B2C) and this could be a consumer paying a business or vice versa.

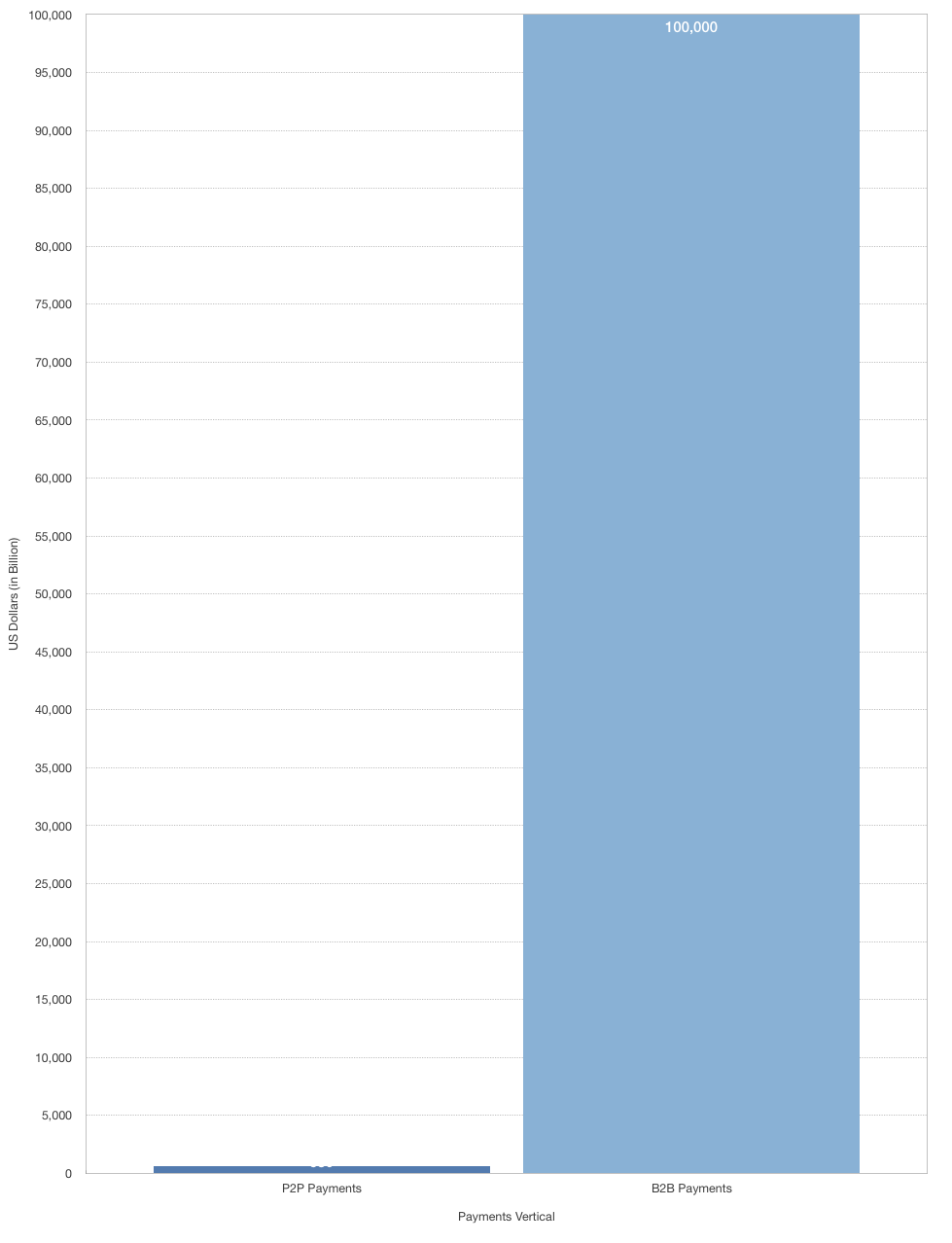

Start looking at handling business payments. What would it mean from an on-boarding point of view? From a compliance point of view? From a partner-network point of view? There is a HUGE difference between the $630 Billion remittance industry and $100+ Trillion B2B payments industry.

To put that into perspective…

The P2P market has about 8,000-10,000 players (not counting banks) and the B2B market has about less than 750 players (again, not counting banks).

Where do you think more opportunities lie? It does not have to be either/or. You can comfortably service both markets with slight adjustments on your front & back office.

Companies big and small today are trading with each other across border lines more than ever before, thereby increasing the need for cross-border payments. The world is flats, but the payments landscape is not quite flat yet.

Making your systems ready to handle a multitude of payments will be to your advantage.

Q10: It is time to start embracing cryptocurrency?

I get a lot of flak for being a proponent of cryptocurrency. I do have my reservations and opinions (like everyone else) of which cryptocurrency is good, which isn’t. Which one is best suited for task X and which is best for task Y. Despite all this, and looking past the punters and speculators or the myopic articles that keep blaming cryptocurrency for all the ills like money laundering, illicit financing, financing of terrorism, etc. — there is the promise of a technology that is slowly reshaping how we interact with money.

Investing time in understanding cryptocurrency today will not make you like a fool tomorrow. You don’t have to start big. Go very small. Open multiple cryptocurrency wallets, load them up with $10 and send pocket change across the world. See how the system acts and behaves. Until you don’t try it – you will never get the hang of it.

I did this short video on the same topic. Why an understanding of cryptocurrency is critical for your future survival.

Admittedly many people that I have had candid discussions with are afraid of it – because they don’t understand it. They need not be. No one was ever born with all the knowledge. Start reading an article once a day and start watching a video once a day. Imagine your knowledge and understanding after say 6 months.

Learning about cryptocurrency does not mean your money services business will be dealing in it. Just because you are learning how to bake a cake, does not imply that you will become a bakery next, same goes with cryptocurrency.

Play with it. No regulator will stop you. No regulator will fine you. No regulator will give you an enforcement order. As long as you keep this to your personal left, and as a small pilot project, you have nothing to worry about.

An investment made in learning today is a whole lot better than being oblivious about it.

Is there hope?

Of course, there is hope. It would be pointless to write such a log article and not give hope.

Note

Hope comes from collaboration. Leverage the strength of each other in the network that collaborates together.

I’m reminded by this scene in the movie Shawshank Redemption, in a scene with Morgan Freeman and Tim Robbins.

When you are faced with dwindling prospects, even thinking rationally and straight becomes an issue. When you see de novo players around you raising tens of millions of dollars, it is difficult not to be jealous.

Self-pity starts to creep in. Life is suddenly not fair. You start blaming yourself that you’ve been dealt with a sour hand.

There is a saying by the German philosopher Nietzsche (I promise this is the last quote I will use, I think).

Stop!

Don’t go there. If you stop looking into the darkness of the situation you may be in and look at the bright side, there is so much, you, as an individual money transfer operator can do.

Now I will tell you, how to go about it.

The Solution

The solution is simple. It is all about Collaboration and Leveraging the combined resources of each other.

Let me explain. The non-technical explanation can be summarized in the diagram below. If the 7,700 or so small and medium money transfer operators of the world unite together, there is immense power in the network they create.

Whilst such diagrams as the one above may seem cute for purposes of illustration, you must look through and understand the concept. The concept is saying if small players unite. If small players organize themselves and are not afraid of talking to their competitors (of the same size), if they come together as one, they can leverage the power of the network and create a disruptive force for the competition.

To truly understand this concept, look what happened to Uber, or Lyft, or AirBnB or other similar marketplaces. Seemingly disparate and disorganized players – get acclimatized (read: harmonized) under a single brand, unified processes and literally take the carpet out underneath from the incumbent and de novo competitors.

Let’s say as a Money Transfer Operator, you need to buy a chair for your office. If a single person walks into a store to buy an office-chair, there might not be any discounts for that person. But if 50 companies pool their purchasing power to buy 50 office-chairs, you can bet you bottom dollar that you will get a discount. This is how leveraging works. This effect is called the Economy of Scale. (or Economies of Scale).

Here is are the definitions of what Economies of Scale are:

- Investopedia: Economies of Scale

- Wikipedia: Economies of Scale

This is one concept, you have read and understand. For your future may literally depend on it.

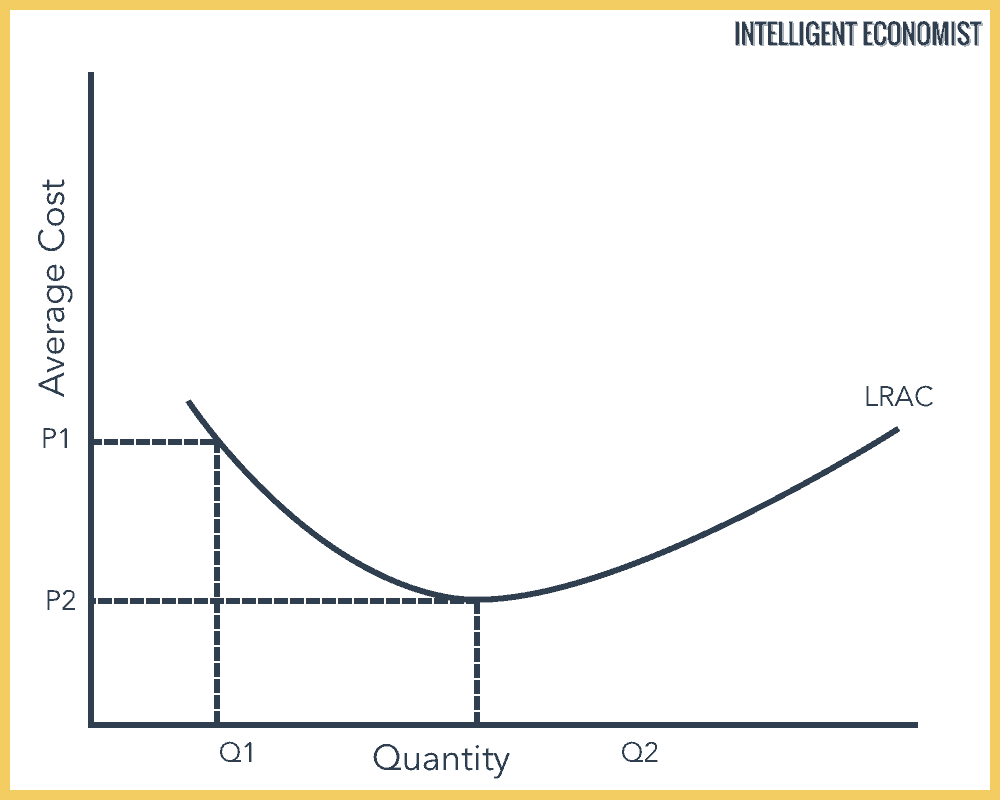

Here is another great article by Intelligent Economist and this graph that pretty much sums it up:

When competing for money transfer businesses collaborate (and we help them do that) then the results are amazing. Suddenly, you have a very large network willing to help out. Networks like BNI and Rotary Club have banked on these ideas for years and have achieved success because of it. Why should the money transfer industry be any different?

The whole idea behind the Uberization of money transfer to bring various money transfer operators under one umbrella and empower them with tools, access to networks, resources and more importantly new business that they never had before. Read this article I wrote a long time ago: The Uberization of Money Transfer.

You need to get out of your comfort zone for this to happen. If it was that easy, it would have happened already.

If you are willing to open up to ideas that can help you elevate your business from where it is, to a playing field you have perhaps only dreamed of.

What do we bring to the table? Lots of things. Technology stack. Information Technology, Access to more banking. Better AML/KYC resources and partnerships, enhanced payment networks and payment processors. Access to different markets. Faster payment rails. Additional transaction types. etc.

How can you participate?

Organize. Leverage. Defeat.

It all starts with filling out this form. Take the first step towards discovering the power of the network.

Open to suggestions

No plan or idea should be so rigid so as not to seek improvement. Mine is no different. If you feel you can contribute towards bettering the idea, please reach out and contact me. If you feel you need to give me some negative criticism, I again invite you to reach out. If you disagree and want to have a healthy discussion on it, again, let me know.

—

This page was last updated on September 1, 2022.

–