One of the strange things about the financial services industry is that, from the outside, it often looks far more connected than it really is.

People assume that because banks exist, payment companies exist, licensed entities exist, and fintech has exploded globally, the system itself must be efficient. In reality, much of the industry still operates through fragmented introductions, private relationships, conference meetings, broker networks, WhatsApp groups, LinkedIn messages, and institutional memory carried around in people’s heads.

Over the years, I kept seeing the same pattern repeat itself.

A company would need an MSB-friendly banking relationship. Another company would need an MTL sponsor. Someone else needed payout infrastructure into a difficult corridor. A crypto company wanted compliant fiat rails. A remittance operator wanted licensing coverage but didn’t know where to begin. Sometimes companies were looking to acquire licensed entities altogether because building from scratch would take years.

In many cases, the solution already existed somewhere in the market.

The problem was never purely lack of providers. The problem was discovery.

Finding the right counterparty in regulated financial services is surprisingly difficult. Not because information doesn’t exist, but because the industry has historically relied on fragmented and highly relationship-driven discovery mechanisms. The right provider may already exist, but identifying who is credible, operationally realistic, regulatorily comfortable, commercially aligned, and actually capable of executing is another matter entirely.

I realized after many years that a large portion of my own work had gradually evolved into operating as a kind of informal market maker.

People would come to me with problems involving banking, licensing, payments, crypto infrastructure, remittance corridors, compliance, or international settlement, and I would try to identify who in the market could realistically help them. Sometimes the solution involved banks. Sometimes it involved licensed entities. Sometimes it involved sponsors, payout networks, crypto infrastructure providers, compliance specialists, or strategic counterparties.

Much of this work happened quietly and manually.

And the more I worked in the space, the more obvious the underlying inefficiency became.

Companies were wasting enormous amounts of time navigating discovery itself. Not execution. Not product development. Not even compliance in many cases. Simply figuring out who the right people were to speak with and how to structure conversations properly.

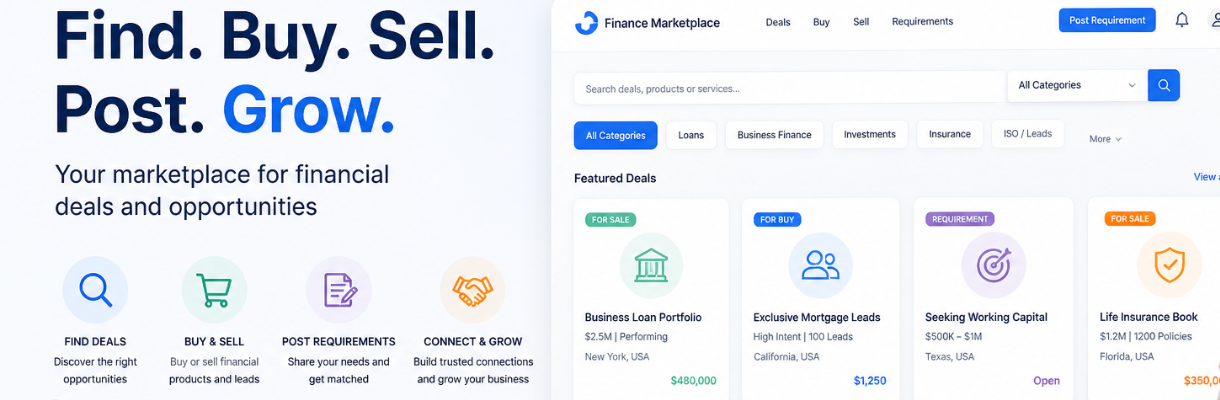

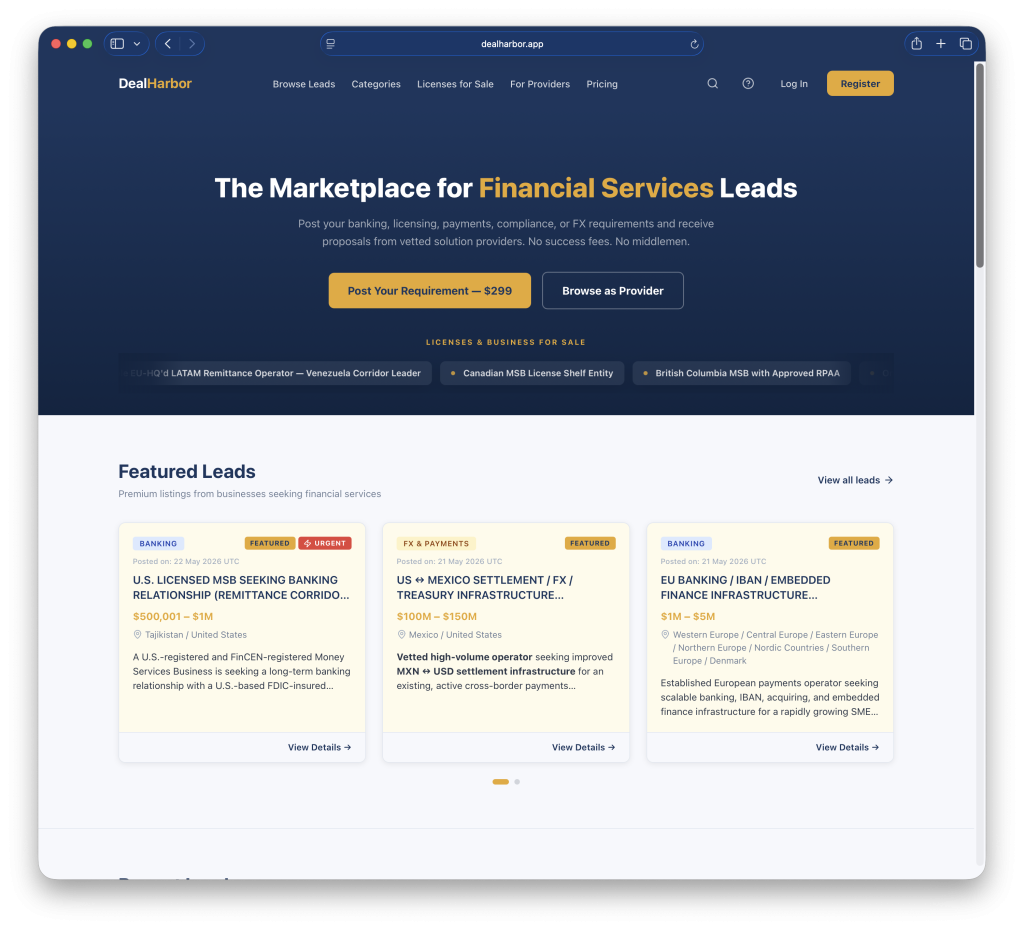

That realization eventually became one of the primary reasons behind building DealHarbor: https://dealharbor.app

DealHarbor is not an attempt to create another generic marketplace or fintech directory. The idea is much narrower and much more infrastructure-oriented than that. The goal is to create a more structured environment for regulated financial services opportunities — particularly in areas like banking, licensing, payments, remittance, crypto infrastructure, compliance, FX, and fintech acquisitions.

The platform is designed around a fairly simple principle: the opportunities already exist, but the discovery layer has historically been fragmented, opaque, and inefficient.

Some opportunities are straightforward marketplace-style listings. Others are more sensitive and are handled through managed placement or private placement structures. In some cases, confidentiality matters significantly because licensing acquisitions, banking relationships, and infrastructure partnerships are not things most companies want publicly circulated without context or qualification.

At the same time, I’ve also become increasingly convinced that the real leverage in financial services often sits beneath the surface layer that most people see.

People tend to focus heavily on:

- apps

- consumer interfaces

- branding

- customer acquisition

But the real infrastructure layer — licensing, sponsor structures, banking relationships, payout rails, corridor access, compliance architecture, and institutional trust — is often where the actual difficulty and long-term value sits.

Those things are not glamorous. They are not always visible. But they are what make the ecosystem function.

And because discovery around that infrastructure layer has historically been so fragmented, entire categories of opportunity remain unnecessarily difficult to navigate.

Whether DealHarbor becomes large or remains niche, I believe the underlying problem is very real.

After years of watching the same friction repeat itself across banking, payments, remittance, licensing, and crypto infrastructure, I eventually decided it was time to stop treating these problems purely as private conversations and start building systems around them instead.

—

DealHarbor is being developed under Misfits.ventures, a venture initiative focused on infrastructure, discovery, and opportunity flow across banking, payments, licensing, remittance, and emerging financial systems.

—

This page was last updated on May 25, 2026.

–