Overview

Amidst Bolivia’s severe dollar shortage, restrictive capital controls, and increasing reliance on informal financial channels, there is a pressing need for legitimate, efficient, and compliant pathways to move money across borders. Entrepreneurs, exporters, and importers alike are seeking mechanisms to bypass the limitations of the local banking system and access U.S. dollars for trade, payments, and capital preservation. This project responds directly to that need by offering a dual-structure payments and compliance framework that enables cross-border settlements via both traditional fiat and crypto rails (specifically USDT).

By combining regulated U.S.-based entities with offshore operational flexibility—backed by expert guidance and access to licensed providers—this solution creates an end-to-end model that is adaptable, fast to implement, and aligned with international financial compliance requirements. Whether the goal is to facilitate named account payments to U.S. vendors, or route payments to non-U.S. destinations such as China, Europe, or Latin America, this platform is built to scale with transparency, legality, and operational efficiency at its core.

Solution Architecture

This cross-border payment solution is structured around a dual-entity framework that enables legally compliant, operationally flexible payments from Bolivia to both U.S. and non-U.S. destinations, using either fiat or stablecoin rails. The structure is designed for B2B and high-value cross-border type payments.

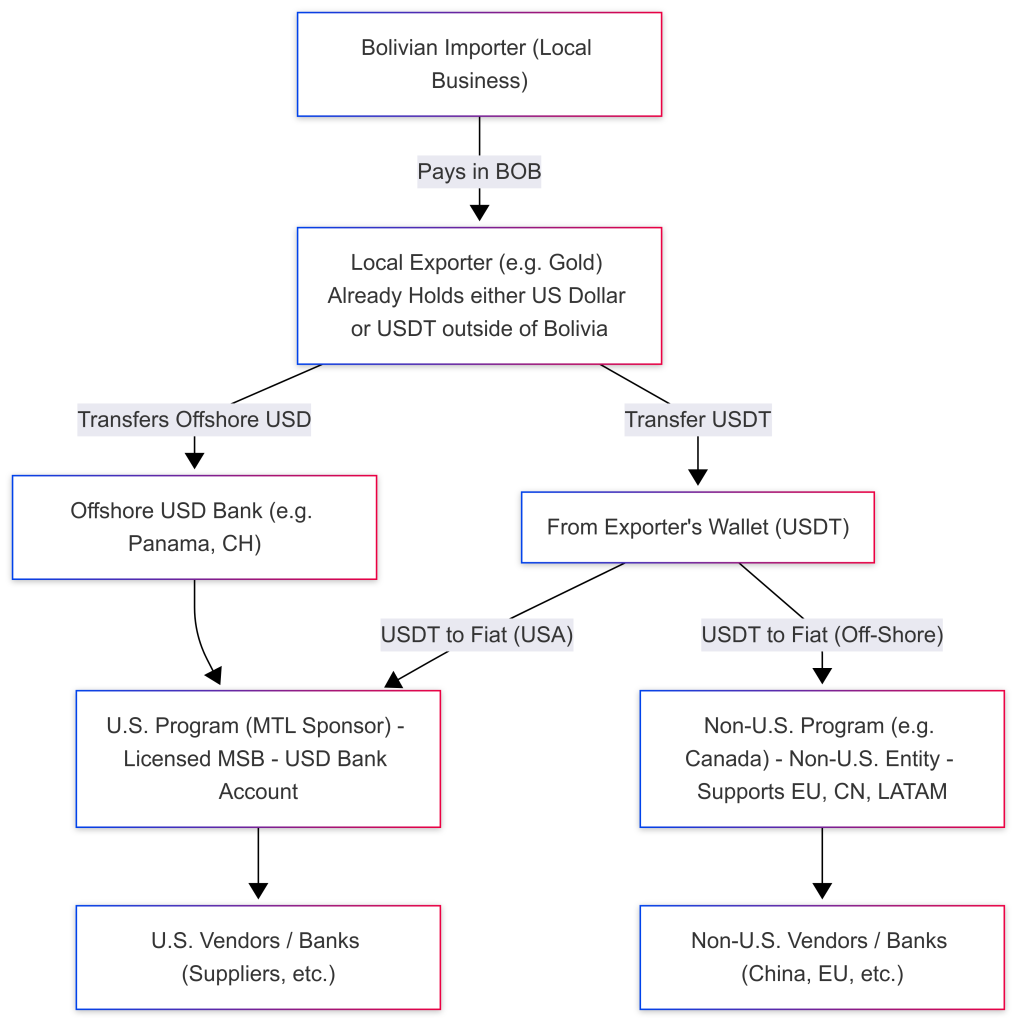

Flow of Funds

Dual-Entity Model

U.S. Entity (Regulated Pathway for U.S.-Bound Transactions)

- Legal Basis: Operates under a Money Services Business (MSB) registration and is covered by a licensed Money Transmitter (MTL) through an agent sponsorship model.

- Functionality:

- Receive USD via wire, USDT liquidation, or conversion

- Settle named or unnamed payments to vendors across the United States

- Maintain compliance logs and regulatory filings (e.g., SARs, CTRs) via sponsor

- Banking:

- U.S. banking is provided via BaaS platform or sponsor’s bank account

- Dedicated sub-accounts for clients may be possible depending on sponsor

Non-U.S. Entity (Flexible International Settlement Path)

- Location: Jurisdictions include Canada (preferred), Malta, Turkey, Panama, or UAE

- Functionality:

- Facilitate transactions that do not touch the U.S. financial system

- Receive funds via crypto or wire

- Pay out to counterparties in China, Europe, LATAM, etc.

- Avoid U.S.-specific regulatory requirements (e.g., FinCEN, OFAC)

- Banking:

- Uses international multi-currency bank accounts or PSPs (Payment Service Providers)

- USDT/USDC-compatible wallets may be custodial or self-hosted depending on risk appetite

Fund Flow Variants

USD-Offshore Flow (Indirect Fiat Path)

- Importer in Bolivia pays a local exporter in BOB.

- Exporter transfers equivalent USD from offshore account (e.g., in Switzerland).

- Funds enter U.S. sponsor bank account or PSP wallet.

- Sponsor entity disburses funds to U.S. beneficiary (e.g., vendor, service provider).

Use Case: Ideal for transactions where importer wants to pay a U.S. entity without going through Bolivia’s central bank.

Stablecoin Flow (USDT Path)

- Importer purchases USDT locally via Binance P2P or OTC desk or local preferred crypto exchange.

- USDT is sent to solution provider’s wallet (U.S. or offshore).

- USDT is liquidated into fiat (via exchange or OTC).

- Fiat is delivered to the end vendor or credited to an IBAN or bank account.

Use Case: High speed, less dependency on correspondent banks, ideal for countries with currency controls.

Non-U.S. Routing Path (Cross-Border B2B)

- BOB is converted into crypto or routed through informal channels.

- Non-U.S. entity receives USD/USDT and disburses payment to Europe, China, or LATAM.

- Payment is made from Canadian, Maltese, or Turkish PSP account depending on geography.

Use Case: Used for payments from Bolivia to Brazil, Argentina, Colombia, Peru, Chile, etc. where U.S. regulation is unnecessary or undesirable.

Compliance Layer

- U.S. Entity:

- Covered under MTL licensing of sponsor

- AML policies enforced by the sponsor

- Monthly, quarterly reporting (dependent on state and FinCEN)

- KYC/KYB managed via integrated onboarding partner (e.g., Alloy, SumSub)

- Non-U.S. Entity:

- Follows local AML/KYC regulations (e.g., FINTRAC in Canada)

- May use custodial or decentralized wallets depending on local law

- Provides auditability, but no U.S. data-sharing requirement unless involved with U.S. banking

Technical Infrastructure Options

- Custody: Hosted wallet providers, cold storage, or hybrid models (e.g., Fireblocks)

- KYC Integration: Document upload + sanctions screening

- Transaction Monitoring: Real-time rules engine for velocity, fraud, and sanctions triggers

- Accounting: Sub-account ledgering for reconciliation of inbound/outbound flows

Scalability Notes

- Suitable for MVP starting at $500K/month

- Scales cleanly to $10M+/month with better pricing, vendor trust, and liquidity access

- Modular expansion: additional corridors can be layered with provider consent

Client Advisory Fee (Faisal Khan LLC)

To assemble either the U.S. program, the non-U.S. program, or both, our consulting fee is US$15,000, covering:

- Flow structuring and entity mapping

- Partner sourcing (MTL sponsors, processors, compliance teams)

- Documentation and onboarding materials

- Strategic advisory for 60 days post-launch

Payment Terms:

- 50% upfront to begin work

- 50% upon signing with the selected solution provider

You will also receive:

- A licensing comparison matrix (own license vs. agent/API sponsorship)

- Estimated costs and processing timelines

- Best-practice playbooks on compliance and fund flows

Probability of Success:

Estimated at 95% based on experience and vetted partner access.

Money-Back Guarantee:

If no solution provider is secured within 120 days, your entire advance will be refunded, no deductions.

Solution Provider Pricing (Estimated Commercials)

The following are estimates only. Final pricing and obligations are outlined in the solution provider’s commercial term sheet.

- Transaction Fees: 0.15% to 1.0% depending on provider; typical: 0.5%–0.75%

- Sponsorship/Agent Setup Fees: $5,000 to $25,000 (most common: $10,000–$15,000)

- Monthly Operations Fees: $3,000 to $5,000/month

- Ancillary Costs (Named Accounts, Compliance Officer, additional corridors): May apply depending on your use case

Coverage includes: Argentina, Brazil, Ecuador, Colombia, Peru, Chile, and more. Expanding to a new country may trigger added compliance review costs.

Context: Obtaining a U.S. MTL in all 50 states can cost $2.2 million and take up to 2 years. This solution gives you nearly instant access via sponsorship—legally, scalable, and at a fraction of the cost. (Click Here to See US Money Transmitter License Application Filing Pricing). Learn more about the different License Options (advantages & disadvantages) between Applying for your own Money Transmitter License vs. Being an Agent (Authorized Delegate) vs. API Relationship.

Frequently Asked Questions (FAQ)

Yes, provided the U.S. arm operates under an MSB registration and licensed MTL sponsor. The offshore arm adheres to the legal frameworks of its respective jurisdiction.

Operating without licensing in the U.S. can lead to jail time, asset seizure, or de-banking. Working under licensed structures eliminates this risk.

No. Operations can be conducted remotely, provided proper compliance protocols and sponsorship relationships are in place.

Yes, using the non-U.S. entity. Ideal for routes into China, Europe, Brazil, Argentina, Venezuela (for OFAC-exempt food trade), and all other LATAM markets including Ecuador, Colombia, Peru, and Chile.

From gold and silver exporters, remitters, and diaspora. Optionally, USDT can be purchased in-country and converted onshore.

Importers who need access to USD, exporters who receive offshore USD, and individuals looking to safeguard their savings or conduct cross-border trade.

No, but it is increasingly common in Bolivia. Stablecoins allow for faster, traceable settlements with reduced counterparty risk.

Roughly $2 million per month. Below that, the operating cost of compliance and sponsorship may outweigh the returns.

Yes. We offer turnkey assistance with LLC/IBC formations, account opening, compliance onboarding, and flow structuring.

We support named accounts, allowing the U.S. payment to reflect the actual importer’s entity name—important for customs, invoices, and AML compliance.

Significant capital strength and customer base are required. Typically, providers expect:

– A community of at least 1,000 active accounts

– Minimum cumulative deposits of $2 million

Without this scale, BaaS providers may decline onboarding or offer only limited functionality.

Absolutely. There’s strong market demand for multi-currency wallets, digital debit cards, and the ability to store, send, and receive funds globally—bypassing fragile local banking systems. With the right setup, this operation can become a trusted alternative to traditional banking.

This is a common challenge. While Minimum Viable Product (MVP) models exist, the market sets baseline infrastructure expectations. For example, processing just $200K–$300K/month—even at a 2% spread—only yields $6K/month in gross revenue, which limits your operational capacity. The real advantages begin to emerge at $2M+/month in volume, where you gain access to better pricing, credibility, and system efficiencies.

If you’re acting as an agent under someone else’s license, you will not need to post your own surety bond. However, if the sponsor requires an increase in bond coverage due to your transaction volume, you may be asked to cover the incremental premium.

Disclaimer

The contents of this document are provided for informational and strategic planning purposes only. Nothing contained herein constitutes legal, regulatory, tax, or financial advice. All clients are strongly encouraged to obtain independent legal and compliance counsel before engaging in any cross-border or regulated financial activity.

All commercial terms, pricing estimates, and licensing structures described are based on prior engagements and current market norms, but are subject to change at the discretion of third-party solution providers. Final terms will be provided directly by the licensed partners or institutions involved.

Faisal Khan LLC is not a licensed financial institution, money services business (MSB), or law firm. Any introductions, structuring support, or advisory services provided are conducted under a consulting capacity only.

Every effort has been made to ensure the accuracy of the information presented; however, Faisal Khan LLC disclaims any liability for errors, omissions, or the outcomes of decisions based on this document. Clients are advised to perform their own due diligence before making any commitments.

Map Out Your Bolivia-to-Global Payment Framework

Ready to build your cross-border payment system? Book your strategy call now.

—

This page was last updated on July 23, 2025.

–