Executive Summary

Iraq and Libya operate unique oil revenue distribution systems where petroleum earnings are allocated directly to citizens through government-issued debit cards. However, unfavorable official exchange rates have created a sophisticated cross-border payment processing industry. Citizens bypass poor official exchange rates by traveling abroad to process their cards through international POS networks, accessing cash at more favorable market rates. This system operates at massive scale—processing $1.5-8 million daily—with standardized 2.5% commission rates across a network spanning Turkey, Dubai, and other international hubs.

Key Findings

Scale: Daily processing volumes range from $1.5 million (low traffic) to $8 million, averaging $2-5 million per day.

Commission Structure: Industry-standard 2.75% to 2.95% commission rate, fixed by international market consensus and universally maintained across all participants.

Geographic Network: Operations span Turkey, Dubai, Lithuania (previously), and other international locations.

Payment Methods: Citizens receive oil revenues via immediate cash, USDT/USDC cryptocurrency, or gold purchases.

Overview: Oil Revenue as Citizen Entitlement

The Fundamental Premise

In Iraq and Libya, oil revenues are constitutionally recognized as belonging to the citizenry. These governments have established direct distribution mechanisms where petroleum earnings are channeled to citizens through government-issued debit cards (Visa/MasterCard). This represents a form of sovereign wealth distribution directly to the population rather than through traditional government spending channels.

The Exchange Rate Challenge

The core problem driving this entire system stems from significant disparities between official and market exchange rates. While actual rates vary by country and fluctuate over time, the following illustrative examples demonstrate the substantial differences:

- Official Government Rate: $1 USD = 10 Local Currency Units

- Open Market Rate: $1 USD = 20 Local Currency Units

- Rate Disparity: Citizens can potentially double their purchasing power

Note: These are fixed illustrative rates used for demonstration purposes. Actual exchange rates differ for each country and change based on market conditions.

The Local Usage Problem

When citizens attempt to use their oil subsidy cards domestically within Iraq or Libya, they are constrained to the official government conversion rate. This forces them to accept significantly reduced value for their rightful oil revenue allocations. The government-controlled exchange rate typically offers substantially less favorable terms than what the same currency would fetch in open market transactions.

The International Processing Solution

By processing cards internationally through courier networks, citizens can receive US dollars directly. These dollars can then be exchanged in their home country’s informal currency markets at the more favorable unofficial rates. This process allows citizens to access the true market value of their oil revenues rather than accepting government-imposed conversion rates that diminish their purchasing power.

This fundamental economic arbitrage opportunity—the difference between official and market rates—creates the entire foundation for the cross-border processing industry.

The Economics of Citizen Participation

Why Citizens Choose International Processing

The decision for Iraqi and Libyan citizens to utilize international courier services stems from compelling economic incentives that far outweigh the associated costs and complexity. Citizens face a stark choice: accept substantial financial losses through domestic card usage or invest in international processing to maximize their oil revenue value.

Economic Motivation Analysis

- Domestic Loss: Using cards locally can result in 50-100% value reduction due to poor official exchange rates

- Processing Investment: 2.75-2.95% commission plus courier tips ($25-50)

- Net Benefit: Despite processing costs, citizens can potentially double their purchasing power

- Risk Assessment: Many citizens view the international processing route as essential financial protection

Trust and Necessity Factors

Citizens often lack the knowledge, resources, or capability to navigate international payment systems independently. The complexity of international travel, regulatory compliance, currency declaration procedures, and POS network access creates dependency on specialized courier services. For many citizens, particularly those in remote areas or with limited international experience, trusted courier agents represent the only viable path to accessing fair market value for their oil revenues.

The Courier Journey: International Operations

Pre-Departure Preparation

Courier agents begin operations by collecting oil subsidy cards from citizens across Iraq and Libya. This collection process involves extensive coordination, as agents must gather not only the physical cards but also critical transaction data for each card. Citizens provide their PIN numbers and specify exact amounts they wish to process, creating detailed transaction manifests that agents must carefully manage and protect during international travel.

Travel Logistics and Documentation

The international journey requires meticulous planning and compliance with multiple regulatory frameworks. Courier agents must ensure proper documentation for:

- Card Transportation: Carrying hundreds of cards across international borders

- Financial Declarations: Preparing for potential currency declaration requirements upon return

- Business Documentation: Maintaining legitimate business purposes for travel

- Communication Systems: Establishing secure channels with processing centers and clients

Destination Selection Strategy

Agents strategically choose processing destinations based on multiple factors including regulatory environment, POS network availability, settlement speed, and operational costs. Turkey and Dubai have emerged as primary hubs due to their business-friendly regulations, extensive financial infrastructure, and geographic proximity to Iraq and Libya.

Detailed Transaction Processing Workflow

Card Collection and Organization

Batch Assembly Process

Courier agents typically work with batches of 200+ cards per processing trip, though volumes can vary significantly based on demand and operational capacity. Each card in the batch comes with specific processing instructions:

- Card Identification: Physical card with embedded chip and magnetic stripe

- PIN Information: Four-digit personal identification number provided by citizen

- Transaction Amount: Specific dollar amount to be charged (ranging from $1,000 to $8,000+ per card)

- Client Instructions: Any special requirements for payment method (cash, crypto, gold)

Security and Organization

Managing hundreds of cards with associated PINs and transaction amounts requires sophisticated organizational systems. Agents must maintain accurate records while ensuring security throughout the international journey. Cards are typically organized by transaction amount, payment preference, or processing priority to streamline operations at destination processing centers.

International Processing Center Operations

Facility Infrastructure

Processing centers operate sophisticated infrastructures designed for high-volume card transactions. These facilities typically maintain:

- Multiple POS Terminals: 20+ machines operating simultaneously

- Business Registrations: Legitimate merchant accounts under various business categories

- Staff Coordination: Teams of operators managing concurrent processing streams

- Cash Management: Secure cash handling and storage systems

- Settlement Infrastructure: Multiple payment method capabilities

The Processing Sequence

Step 1: Initial Card Verification

Upon arrival at processing centers, courier agents begin systematic card verification. Each card undergoes preliminary checks to ensure chip functionality, magnetic stripe integrity, and account accessibility. This verification process helps identify any problematic cards before full processing begins.

Step 2: POS Terminal Assignment

Cards are distributed across multiple POS terminals to maximize processing efficiency. Different terminals may be assigned based on transaction amounts, payment methods, or specific business merchant categories. This distribution strategy helps avoid detection patterns and ensures smooth processing flow.

Step 3: Individual Transaction Processing

Each card undergoes individual processing through the following detailed sequence:

- Card Insertion/Tap: Physical card presented to POS terminal

- PIN Entry: Four-digit PIN entered by processing center operator

- Amount Entry: Specific transaction amount input (e.g., $3,500)

- Transaction Authorization: Real-time communication with card issuing bank

- Approval Confirmation: Transaction approved and processed

- Receipt Generation: Transaction record created and stored

Step 4: Immediate Settlement Protocol

The critical differentiator in this system is the immediate settlement requirement. Unlike traditional merchant processing with delayed payouts, this system operates on instant settlement:

- Immediate Cash Payment: $3,500 charged = $3,500 cash immediately provided

- No Batch Processing: Each transaction settled individually, not at end of processing session

- Real-Time Liquidity: Processing centers maintain substantial cash reserves for instant payouts

- Commission Deduction: 2.75-2.95% commission deducted from each transaction immediately

Payment Method Options and Execution

Cash Settlement Process

When couriers choose cash settlement, processing centers provide immediate USD cash payment for each transaction. This requires processing centers to maintain significant cash reserves and sophisticated cash management systems. Cash payments are counted, verified, and secured immediately upon each transaction completion.

USDT/USDC Cryptocurrency Conversion

For clients preferring cryptocurrency, processing centers facilitate immediate conversion of cash proceeds into USDT (Tether) or USDC (USD Coin) stablecoins:

- Conversion Execution: USD cash converted to USDT at current market rates

- Wallet Transfer: USDT transferred to courier agent’s designated wallet address

- Transaction Confirmation: Blockchain confirmation provided as receipt

- Wallet Security: Agents maintain secure cryptocurrency wallets for client funds

Gold Purchase and Storage

Gold represents a popular value storage and transport option:

- Precious Metal Acquisition: USD proceeds used for immediate gold purchases

- Purity Verification: Gold tested and certified for purity standards

- Secure Packaging: Gold prepared for secure international transport

- Documentation: Purchase receipts and authenticity certificates provided

Return Journey and Client Settlement

Value Transport Security

Courier agents face significant logistical challenges in transporting value back to Iraq and Libya. Whether carrying cash, gold, or managing cryptocurrency wallets, agents must navigate international customs, declaration requirements, and security considerations.

Currency Declaration Compliance

Large cash movements require proper declaration procedures at international borders. Agents must maintain detailed documentation showing legitimate business purposes and comply with all currency declaration requirements. This process, while adding complexity, ensures legal compliance and smooth border crossings.

Final Client Settlement

Upon return to Iraq or Libya, courier agents complete the value chain by distributing proceeds to citizens:

- Commission Deduction: 2.75-2.95% commission plus agreed tips ($25-50 per card)

- Exchange Rate Application: If converting USD to local currency, competitive unofficial rates applied

- Final Payment: Citizens receive maximum value for their oil revenue through optimized exchange rates

This comprehensive process, while complex and requiring significant coordination, enables Iraqi and Libyan citizens to access fair market value for their government-provided oil revenues, circumventing restrictive official exchange rates that would otherwise diminish their purchasing power substantially.

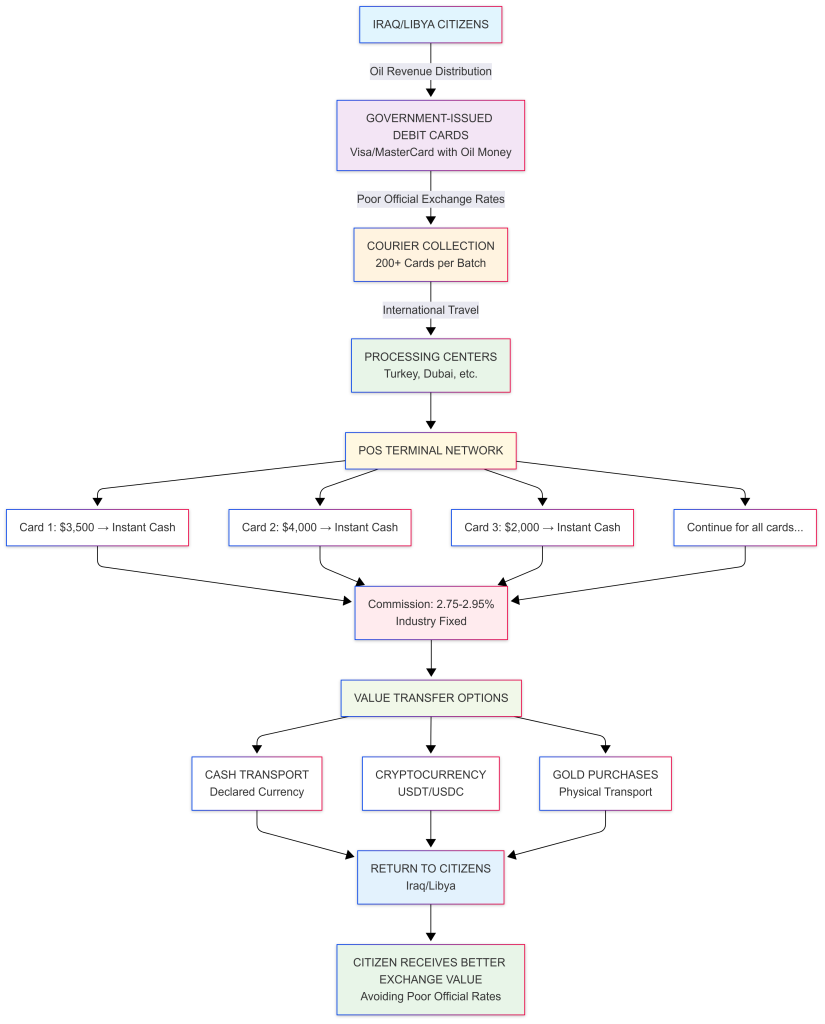

Operational Framework

The system operates through a network of couriers, processors, and international POS terminals that enable citizens to access their oil money at more favorable exchange rates.

Transaction Process Flow

Step 1: Courier Collection

- Couriers from Iraq/Libya collect batches of citizen debit cards

- Typical batch size: 200+ cards per courier

- Each card contains: PIN number and desired charge amount

- Cards are pre-funded with oil revenue allocations

Step 2: International Processing

- Couriers travel to processing centers (primarily Turkey, Dubai)

- Cards are processed through multiple POS machines

- POS terminals sourced from various businesses (restaurants, car washes, gold dealers)

- Each transaction processed individually with immediate cash payout

Step 3: Immediate Settlement

- Cash provided instantly upon each card transaction

- No batch processing delays—payment occurs per transaction

- Example: $3,500 card charged = $3,500 cash immediately provided

Step 4: Value Transfer

- Couriers return value to citizens through three primary methods:

- Cash: Declared currency transport back to origin country

- Cryptocurrency: USDT/USDC purchases for digital transfer

- Gold: Physical precious metal purchases for transport

Economic Structure and Participants

Commission Framework

The industry operates on a standardized commission structure that is internationally market-determined and strictly maintained across all participants:

- Rate Range: 2.75% to 2.95% – fixed by international market consensus

- Market Standardization: All participants strive to operate within this established range

- Participant Distribution: Commission covers all network participants

- Additional Revenue: $25-50 tips per card common for courier services

Network Participants

Primary Stakeholders

- Card Providers: Source pre-funded cards from Iraq/Libya

- Couriers: Transport cards and facilitate processing

- Processing Centers: Operate POS networks internationally

- Business Entities: Provide POS terminal infrastructure

- Citizens: Ultimate beneficiaries of oil revenue distribution

Geographic Operations and Infrastructure

International Processing Centers

Turkey: Primary processing hub with extensive POS networks Dubai: Major operational center with business-friendly regulations Lithuania: Previously operational (shut down due to regulatory changes)

POS Network Structure

Processing centers maintain extensive POS terminal networks:

- Capacity: 20+ machines per processing center

- Business Integration: Terminals registered under various business types

- Transaction Types: Card-present transactions with PIN verification

- Volume Capacity: Support for high-frequency, high-value processing

Regulatory and Compliance Considerations

Currency Declaration Requirements

Large cash movements are facilitated through proper declaration procedures:

- Legal Framework: Declared currency transport is permitted

- Documentation: Proper customs and financial declarations required

- Compliance: Operations maintain legal currency movement protocols

Business Registration

POS terminals operate under legitimate business registrations:

- Cover Businesses: Gold dealers, restaurants, car washes, various retail

- Regulatory Compliance: Proper merchant account establishment

- Transaction Legitimacy: Card-present transactions with PIN verification

Market Analysis and Volume Assessment

Daily Processing Volumes

- Low Traffic Days: $1.5 million Average Days: $2-3 million

- High Volume Days: $5-8 million Consistency: Daily operations with continuous processing

Market Demand Factors

- Population Scale: Large citizen base eligible for oil revenue distribution Economic Incentive: Significant exchange rate arbitrage opportunity

- System Reliability: Established network with proven processing capability Geographic Accessibility: Multiple international processing locations

Key Success Factors

Operational Requirements

- Immediate Settlement: Cash-on-demand payment structure essential

- Pre-funding Capability: Processing centers require immediate liquidity

- Geographic Distribution: Multiple international processing locations

- Compliance Infrastructure: Proper regulatory and documentation frameworks

Critical Dependencies

- Exchange Rate Differentials: System viability depends on official/market rate gaps

- Regulatory Stability: International processing centers require stable operating environment

- Transportation Infrastructure: Reliable courier networks for card and value transport

- POS Network Maintenance: Continuous terminal availability and processing capability.

Conclusion

Iraq and Libya’s oil revenue distribution systems represent unique approaches to sovereign wealth sharing that have generated sophisticated cross-border payment processing networks. The substantial exchange rate differentials between official and market rates have created a thriving industry that processes millions of dollars daily while providing citizens with significantly better value for their oil revenue entitlements.

The system’s success relies on standardized commission structures, reliable international processing infrastructure, and proper regulatory compliance frameworks. As these mechanisms continue to evolve, they offer insights into innovative approaches to citizen benefit distribution and the emergence of alternative financial networks in response to traditional banking limitations.

Understanding these systems provides valuable perspective on how economic policies, exchange rate management, and citizen benefit programs can drive the development of alternative financial ecosystems that operate across international boundaries while maintaining legal compliance and operational efficiency at industry-standard commission rates ranging from 2.75% to 2.95%.

Ready to explore this model?

Want to replicate this card processing system in a currency-restricted market? Schedule a free 15-minute call to discuss feasibility, risks, and setup.

—

This page was last updated on July 25, 2025.

–