How the mobile phone is transitioning from a delivery channel to a payment instrument.

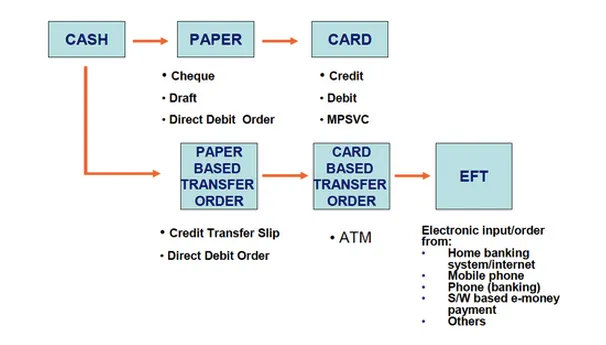

A little over 60 years ago, Frank McNamara forgot his wallet at dinner at Major’s Cabin Grill restaurant in New York. Luckily, Mr. McNamara’s credit and reputation was good at the restaurant, that he was able to pay later. That moment in history was what led to the creation of the credit card, namely the Diner’s Club International card (aptly named after the experience).

At that point in time, the card was not considered a payment instrument. It was a delivery channel. The cards was a means to deliver product/services and pay for it. Fast forward to today, the plastic credit card you and I carry, is a payment instrument. It is money.

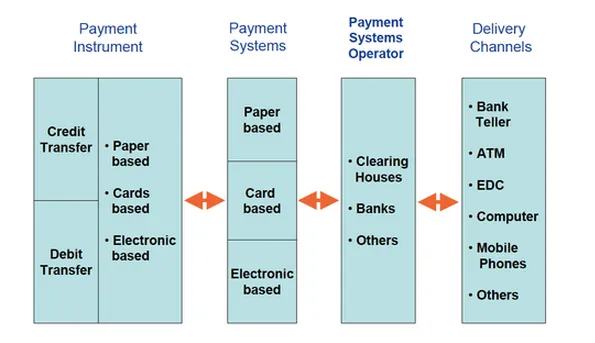

What exactly is a payment instrument? a Delivery Channel? In the classical sense, it can best be described by the diagram below.

The bank teller, the mobile phone, the Internet banking we use, are all delivery channels. 60+ years ago, Frank’s newly embossed card was also a delivery channel. Somewhere along the line, with mass adoption, the card transitioned from a delivery channel to a payment instrument.

Just to expand on the Payment Instrument section, this is how a modern-day payment instruments are defined.

Circa 2000 our mobile phones were just great at making us communicate with each other. Texting was perhaps the only native application that one could use on the phone. Towards the middle of the decade, Blackberry’s influence was coming out strong. Now email, web and a couple of communication apps were taking stage.

All this was about to change. On 29th June, 2007, the world as we knew it, experienced disruption. Steve Jobs introduced the iPhone.

The floodgates of opportunity were opened.

The rest as they say, is history. We have transitioned exponentially since 2007. The mobile phone today is part and parcel of what I would call “me”. It defines who “I” am. In some crude manner, it is an extension of who I am.

The delivery channel called mobile is today enabling us to send a text message to have a vending machine drop a can of soda. We can use the same SMS text over a secure channel (USSD) and do banking. Case in point, M-Pesa. It can check our email. Authenticate us. Identify us. Keep a track of where are. Keep a track on our expenses. Take photographs. Play Games. Listen to music. Play videos. Surf the web. It does it all.

With the advent of the card reader by Square, the mobile space changed overnight. The mobile phone became the POS terminal.

Now, everyone business, big or small had the capability to accept credit card payments. This was the equivalent of serving the unbanked in the banking space or what I called, the unmerchants.

Fast forward to today. The mobile phone is a powerful, multi-facet computing, communicating and transacting device. It is fast taking on multiple roles. Perhaps the biggest role it is adapting to right now is the wallet.

The mobile phone is the wallet.

For millions of people across the world, it is a wallet that allows one to store money inside of it as well as connect money to it. It is seen by many still as a delivery channel, but is it?

For example, the world’s largest mobile wallet company is Tencent out of China (no, its not PayPal).

WeChat which is Tencent’s flagship mobile app, offers ubiquitous banking and payments for all WeChat users. Irrespective of the mobile carrier they use or the bank. The WeChat wallet allows you to seamlessly attach your money to your mobile phone. Paying each other is as simple as sending a text message. That is how easy, simple and frictionless payments have become, for us.

For the Gen Y, mobile payments is the most preferred way of paying. It is no surprise that almost every conceivable company, bank, telco, etc. is positioning itself towards the mobile wallet. Why? Because in 10 years from now, the mobile phone will be a payment instrument. Millions of people who otherwise would not have banked, are banking, paying and transacting using the mobile phone.

A colleague of mine recently cited…

“Email killed the fax machine, mobile phone killed the landline, and mobile wallets will kill the traditional bank-branch”.

I agree. Just as the younger generation of today has gravitated towards their mobile phones for all things considered, the digital evolution would be that the physical wallet will eventually disappear. The wallet for money and identity will be 100% mobile. 100% digital. 100% ubiquitous.

As a payments consultant, I have hammered this concept into my clients, day in and day out. Sadly, most do not subscribe to the gravity of the opportunity here. Banks and businesses who continue to give second preference to mobile wallets, would lose out on the early adoption.

In a recent post (Facebook forays into the world of online payments?), I cited how Facebook has slowly acquired money transmitter licenses for all the US States, as well as securing licenses in Ireland and UK (which would allow them access to EU markets also). The $19 Billion acquisition by Facebook of WhatsApp is no accident. The separation of Facebook Messenger as a separate division is intentional. What is Facebook aiming at? FB is looking at the messaging layer (be it Facebook Messenger or WhatsApp) as the native payment layer on your mobile device. The messaging layer will become mobile wallet (layer).

Contact lists are fast becoming the de facto method of selecting someone to pay. Who else manages contacts better than a messaging app? Those who will eventually control a large swatch of messaging app users, will control the payment space. The wallet would be embedded within the app, allowing you to attach any payment instrument, hence making your mobile a payment instrument itself.

You could have bank cards, credit cards, bank accounts, loyalty cards, etc. all on a singular device, authenticated by your fingerprint, retinal scan or even by your voice print. Paying would be synonymous to sending a message. Select person, amount, authenticate and Send! Voila!

The days of the physical card are indeed limited. Card giants VISA and MasterCard are now both support HCE or Host Card Emulation, where the need for a physical card is entirely eliminated. PayPal has its wallet. Square has its wallet. ISIS has a wallet. Paym has a wallet. Google has a wallet. Apple almost has a wallet.

The transformation on to the mobile space is much more than a buzzword. It’s fast becoming the mantra in banks and businesses, who have to adopt, in the hopes of surviving this rapidly changing world.

In the end, there will be two parties to this revolution. Those who get it. Those who don’t. Go ahead, hold your phone in your hand. What do you see?

—

This page was last updated on January 13, 2025.

–