If you had asked professionals in the Fintech space about 7–8 years ago, what the word remittances meant, you’d be hard-pressed to find people who could accurately define it for you. Just for the record: I was one of them.

Today, in the so called Post-Bitcoin-Paper published era it is almost impossible not to run into a startup that is not trying to enter into the money-transfer (or remittances) game.

The immediate lure is market size: US$500+ Billion is huge. Everyone is thinking, if my startup can get 1/10th of 1 percent, this means, we would be processing $500 Million a year. Sounds sweet don’t it?

Well, there are always two sides to a story. Remittances, money transfers, person-to-person payments, etc. will eventually all just merge. It will just be payments. Whether you are sending money across the world or across the room, the process would be simpler and singular.

This article briefly highlights some of the not-so-obvious challenges that startups in the money transfer business will face.

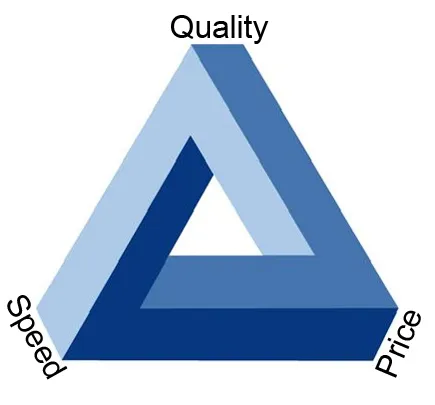

The Triangle of Choice

In my daily life, I come across a lot many companies and individuals who are trying to crack the remittance market.

It’s the gold rush, all over again!

Each aspiring player has their own unique payments DNA on how to best tackle the money transfer market. The goals of all the solutions are typically focused on three areas:

- Speed

- Value

- Comfort

Funny enough, this reminds me of the choice triangle I saw some 20 years ago, which is as follows:

The triangle above represents the remittance product. You can pick any two elements and the third element goes against you:

- High Quality (Comfort) + Faster Speed = Increased Price (Value)

- High Quality (Comfort) + Low Price (Value) = Low Speed

- High Speed + Low Price (Value) = Low Quality (Comfort)

Whilst, it looks easy, the remittance game has many variables to it. To try to offer a product that is instant (speed) and you charge (low value) for it – the downside is the low comfort. The comfort can be translated to the MTO pre-funding the account (hence low comfort) or the inability to do this transaction from your handheld device or on the go. You might have to step out and walk into the a physical location of an MTO for this to happen.

Likewise, the other elements in the triangle listed above, come into play equally.

The Floor Value

At what value does the remittance become economical (for all) and yet at the same time, is a viable business product?

This is the proverbial $64 Million question.

With so many players in the game, some say it should be 1% others find the equilibrium at 3% (surely we should not be paying for remittances more than the credit card charges right?).

What happens when Bitcoin comes in to play? The original video of What is a Bitcoin? Cited it being the equivalent of cash for the internet. So if Bitcoin is introduced into the remittance equation, does the over-all cost of the transaction go down? Significantly?

The answer, which may surprise many is, not necessarily so. In most cases, the difference is marginal. Why? Because businesses (and not hobbyists) who want to revolutionize money transfer with Bitcoin, could possibly get away with it for 0.25%, but why should they? How do they make money?

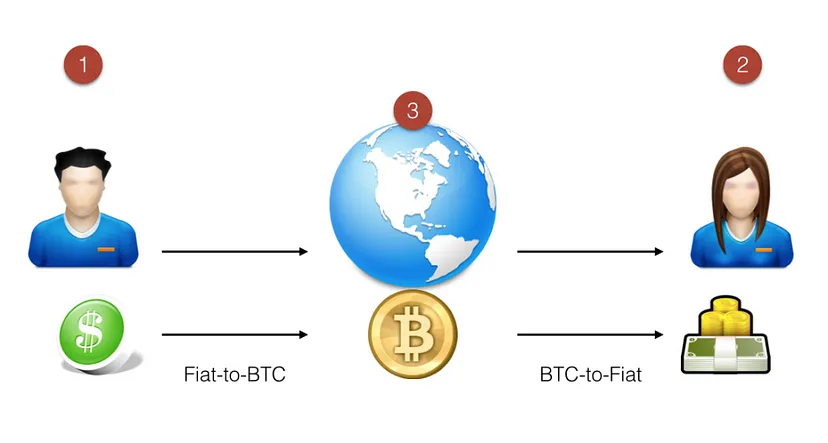

Because the Bitcoin ecosystem is tied to the fiat component on both ends, this means, we have three players who are intricately tied to the system.

- { 1 } Denotes the Send-side party that would have some interest in the transaction.

- { 3 } Denotes the Receive-side party that would have some interest in the transaction.

- { 2 } Denotes the Owner of the system or a middle players (payment network, etc.) that would have some interest in the transaction.

The Owner of the system in most cases have their interested commingled, i.e. {1} + {2}.

Mid-Market FX Gain is usually 2%. At the low end, its 1%, but typically it hovers between 0.75%-to-2.25%, averaging towards the 1.5% mark. If the FX gain is to be 1.5% denoted as {2} above, then components {1} and {3} typically account for 1% each, yielding the total cost of transaction at about 3.5% –

Is this economical? Depends whom you ask and which remittance corridor you are working with.

Competitive Corridors and their Market Share.

If you look at some of the competitive remittance corridors, the pricing on these corridors is extremely competitive. Some examples of competitive corridors are:

- USA-to-Mexico

- UAE-to-India

- UAE-to-Pakistan

- UAE-to-Bangladesh

- UAE-to-Philippines

- Saudi Arabia-to-India

- Saudi Arabia-to-Pakistan

- Saudi Arabia-to-Bangladesh

- Saudi Arabia-to-Philippines

- US-to-UK

- Hong Kong-to-China

- Hong Kong-to-Philippines

- Hong Kong-to-Indonesia, etc.

Most of the above mentioned corridors are operating (for the larger majority) at 2.0% or under. In the case of Middle East to South Asia or Middle East to South East Asia, the competitive nature of the remittance corridor pushes this down to 1%.

100s of Billions of Dollars are transacted through the above-mentioned corridors.

In 2012 (as per World Bank figures) the United States sent US$ 123,274 Million (US$ 123 Billion) in remittances. These are through established money transmitters who having been serving the market for years. The bulk of these remittances are handled by large MTOs like Western Union, MoneyGram, RIA Financial, et. al.

Some breakdown of the corridors:

- US to Mexico: US$ 22,811 Million

- US to Vietnam: US$ 5,679 Million

- US to India: US$ 11,956 Million

- US to Pakistan: US$ 1,094 Million

- US to China: US$ 13,071 Million

- US to Philippines: US$ 10,604 Million

- US to Nigeria: US$ 6,126 Million

Majority of these remittances were in the 1.8% to 2.25% range. A smaller portion was transacted in which the average cost of remittances was less than 1.5%

Breaking into this market, and stealing some market share and at the same time trying to compete will be no easy lunch.

The Real Cost of Being Legal, Licensed & Compliant

If one studies the remittance market in detail, there are tremendous benefits of being a large enterprise. Economies of Scale tilt in your favor. A smaller MTO or a startup MTO will struggle with the following costs:

- Licensing & Costs associated with maintaining these licenses

- Risk Management & Mitigation

- Anti Money Laundering

- Anti Terrorist Financing

- Accounting

- Know Your Customer

- Compliance Reporting

- Cost of Funds

- Back-Office & Settlement functions

- Specialized Personnel

Add these costs to the cost of your product/service development costs, the time lost in going to market, the HR & Office bills you have to pay monthly, becoming profitable in this space is no easy feat.

I personally know of a half-a-dozen companies that were gung ho on specific corridors, but then had to expand massively to other remittance corridors just to cover their costs.

Many realize it late, the Emperor is indeed naked!

Incumbent Players

The incumbents too are keenly watching. They will not be pushed around. I can guarantee you that. Granted there will be a few gains into their respective territories, but the on-ground players (read: distribution partners, payout partners, payout MTOs) who are being offered more by their current partners, seen no commercial benefit in reducing costs for you.

What’s the benefit? Are you asking them to do this for King and Country? Well, better call Saul.

I also see a lot of players, trying to miraculously solve the cost of high-remittances into Africa.

Africa is not the only continent on this planet.

There is a reason why the remittance costs in Africa is high. Its called market monopoly and greed. Plain and simple.

Having reliable, and economical on-ground payout partners is a huge hurdle. This is especially true if your financial model is offering less than what these payout partners were getting before. Long term contractual arrangements with larger MTOs may also prevent them from signing up with you, resulting in you getting 2nd or 3rd tier payout partners, who have limited reach, limited compliance and sub-par service levels.

Key Takeaways

Just because you are a start-up, don’t expect the world to take pity on you and to bestow fortune upon you. It is like the Wild West out there. It is very easy to put numbers in an Excel spreadsheet and see growth. Reality, however, has a very different game in mind for you.

Contracts that are supposed to take weeks, take months. Tie-ups that were so willing to do business with you, become more demanding, the promised transactions that you were to onboard, are not to so easy. The license you thought you’d get, is still a few weeks away. The costs which you had in tight control, seems to be spiraling out of control.

Think before you leap. Think very hard and best of luck.

—

This page was last updated on January 13, 2025.

–