The Decline of Correspondent Banking Relationship

Over the past couple of years, there has been a rapid decline in the offering of corresponding banking relationship (CBR) for non-banking institutions. The money transfer industry has been hard hit. Also affected are licensed payment institutions who have seen correspondent banking relationship drawn away from them. Especially, US Dollar clearing. Is there hope for companies outside the United States to get correspondent banking relationship?

The situation is bleak, but there is hope.

The reduction in correspondent banking relationship accounts has many facets to it and is not something that is going to be discussed here. Suffice to say, compliance, government pressure, derisking from NBFIs, etc. all play a very important part in it.

A new breed of service providers is now in the market to provide alternative CBR accounts, or to put it more accurately, quasi CBR accounts.

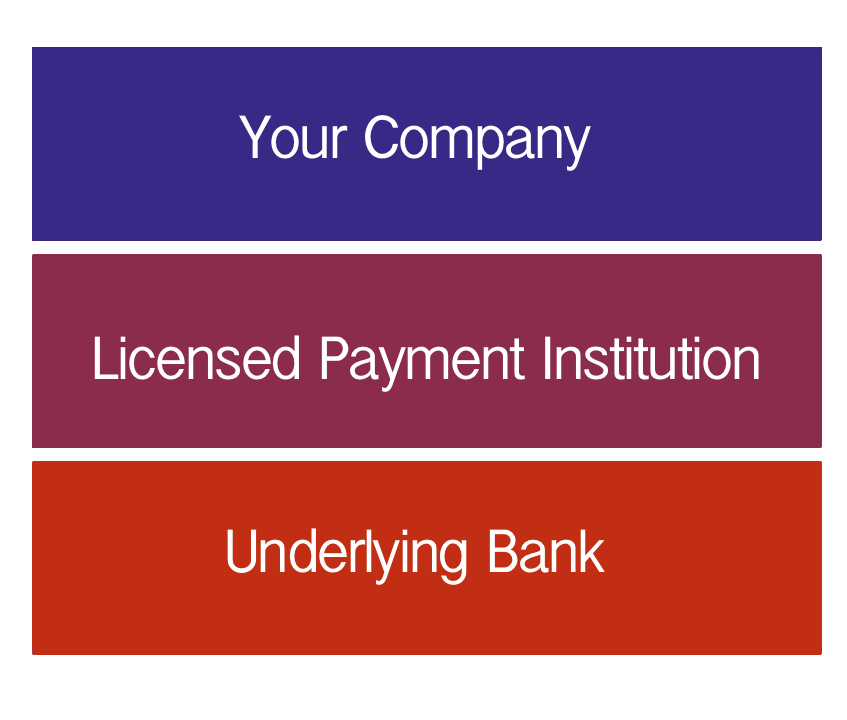

These accounts are known as Virtual IBANs. They are provided as a service by bona fide licensed payment institution entities who have spent lots of money on compliance and relationships with their banks to offer this to 3rd party customers, such as yourselves.

In such a relationship, you will have access to a payment account. A payment account is essentially a bank account, that is run on top of the banking services provided by the underlying bank to the licensed payment institution. You can’t access the bank account directly, but rather through the web/app provided by the payment institution.

You can do electronic receipt of funds, convert currency to other currencies and make payments. You cannot deposit cheques and/or cash. Only electronic payments in and out are supported in this quasi correspondent banking relationship account.

Your clients, suppliers, vendors, principals, etc. are free to send payment to your IBAN account (you will have a separate Virtual IBAN account for each currency).

Likewise, from your IBAN Account, you can send payments to any bank account in the world.

So what’s the catch?

There are a few catches to this quasi correspondent banking relationship account.

- Only business to business payments are supported

- For all payments coming IN, a fee of usually 0.15% (varies between 0.1% to 0.50%) + base fee (between $5 to $25) is charged on all incoming wires.

- Any currency conversion you do, there is a 1.0% FX markup.

- If the payment seems to be coming in from a high-risk client or business, the rates go up. In certain instances, you may even risk account closure (if you are deemed high-risk, forex trading, binary trading, gambling, porn, adult, etc.)

If you’re interested to learn more about quasi correspondent banking relationship accounts, i.e. payment accounts, please click here.

—

This page was last updated on June 19, 2023.

–