Understanding the Behavioral Aspect of Mobile Wallet Commerce — What years of research tells us.

There should be no doubt that as a society, today, we are more dependent on our mobile phones than ever before. Our smartphone represents the core of how we communicate and interact. They are truly an extension of us.

This article aims to provide a thought-provoking look at how we should be addressing mobile money wallets in developing markets. The perspective is a notch above the vanilla roll-outs providers do today. It encompasses both the online and offline world, caters to the problem of cash-only markets where, due to taxation reasoning, merchants are hesitant to accept electronic money and finally addresses the various factors that need to be looked at from a continual engagement point of view, i.e. traction with the ecosystem.

Why read this article? Simple: Obsession!

If you’re not obsessed with every aspect of your product/service, you might as well skip this article. There are two types of visionaries:

- Those who just want a product and place it in the market and go live.

- Those who strive for and achieve perfection. They research their product, which is reflective of what users want and is not based on personal opinions or hearsay.

If you’re the former, might I suggest Imgur to waste time. Else, read on.

Understanding Behavior

The first and foremost understanding is that of Behavior. User adoption and repeated usage of a mobile wallet boils down to behavior. A classical mistake that service providers make is that they ignore behavior, citing it as an unimportant variable to the overall design solution.

Behavior is everything.

If you study behavior and model it, you can work backwards towards a process, yielding to a feature set, which in turn is your solution design.

Spending Personas are different for each user

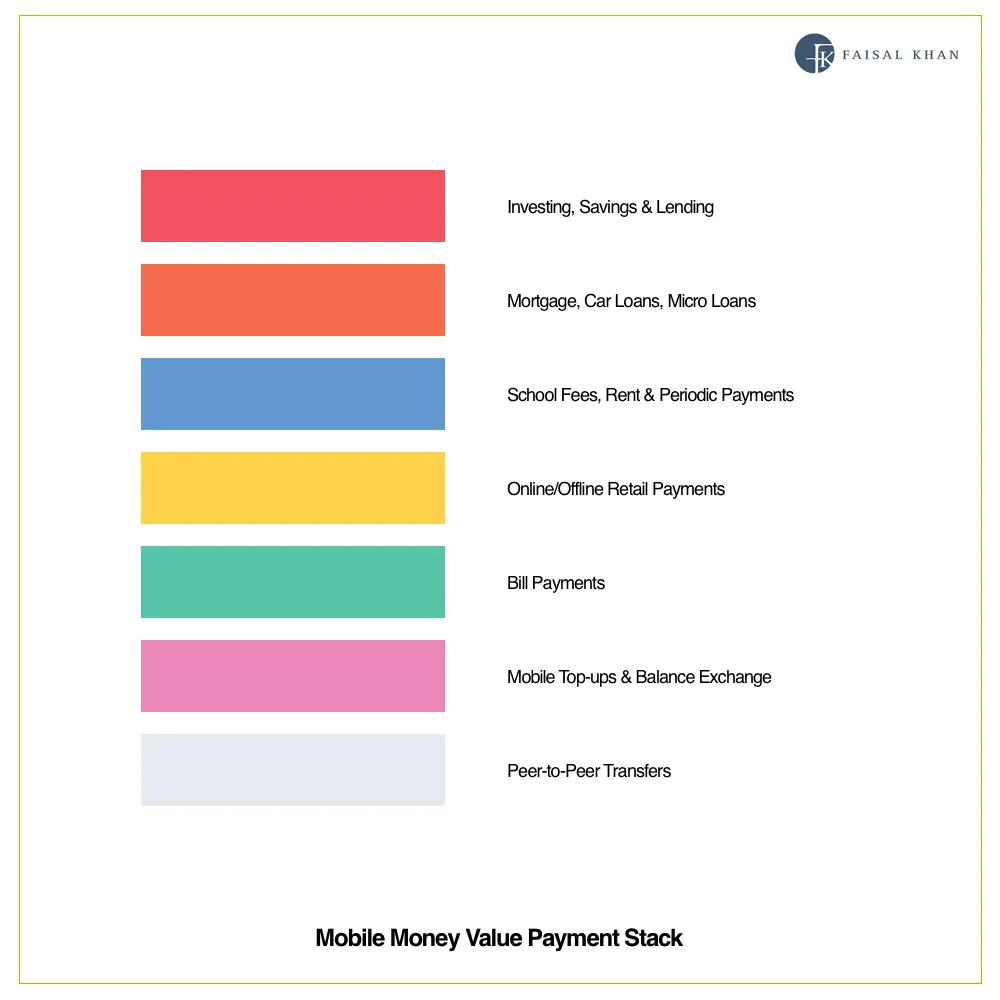

How you and I spend money is extremely different. Mobile Money Operators and Wallet Providers today bank on Person-to-Person (or Peer-to-Peer) transactions as their core business. This is the very bottom of the payment value stack.

The need for P2P transfers will always be there. Consider the following example, a person in CityA sends money to his family in CityB. This is the underlying market that the mobile money operators and wallet providers are interested in. It is simple, fast, no fuss.

However, the scenario becomes interesting when the person at the opposite end receives the money (let us assume, the spouse receives it) then how he/she spends the money is where it gets interesting.

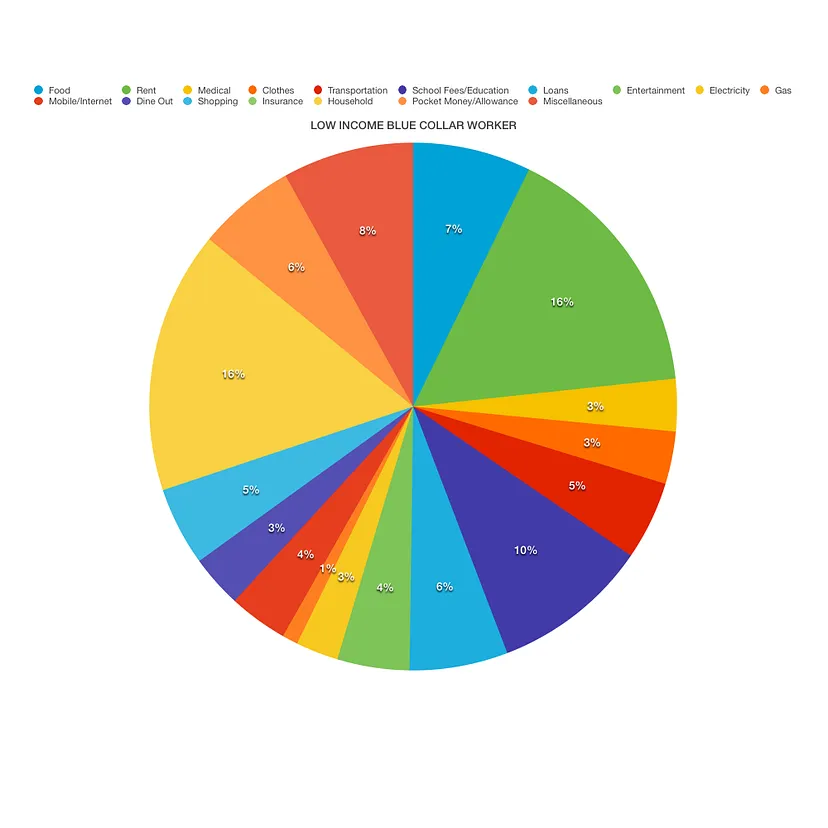

In Pakistan, for example, a typical rural housewife who receives money from her husband does an average of 23 transactions per month with the money (not counting petty cash transactions).

The telco/wallet-operator was only part of one transaction, i.e. when she received the money.

Twenty-two transactions are up for grabs! But they are only available to those who understand how she spends her money.

The fast-food industry is perhaps the best example of a simple vertical that really understands buyer behavior. Behind the scenes, fast-food restaurant chains invest millions in trying to understand the socio-economic (and at times even the socio-political) fabric of the customers they aim to serve. Their deep understanding of user behavior probably far outshines anyone else who has limited access to their customers.

The industry can standardize a product offering, yet still giving the user the ability to customize their order (case in point: Hold the pickles and tomatoes on the Whopper please).

Mapping The Journey

It all starts with focus groups / group discussion.

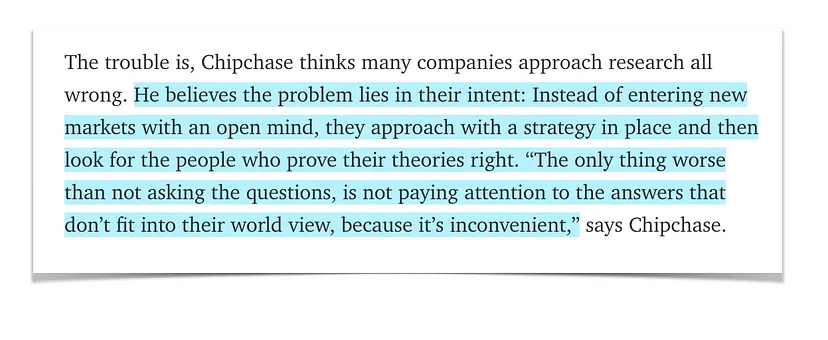

It is imperative that a completely neutral (yet knowledgable) party is involved in conducting the focus group. You have to divorce yourself from the answers or validations that the company seeks, and in turn must start blank (fresh). Do not try to go into a focus group, reiterating what has already been discussed in the boardrooms or points highlighted by your marketing department.

World renowned researcher, designer and strategist Jan Chipchase sums it very well.

Start with a clean slate. Let your users definite what banking, money, mobile money, e-commerce, internet, apps, etc. are. From those definitions, dig deeper:

- What they like / don’t like about certain application or services?

- How important is money to them?

- What is money to them?

- Why do they value money?

- What do they hate about money?

- What do they love about money?

- How do they spend money?

- How do they save money?

- How do they keep track of money?

- What other aspects of money are they aware of?

- What don’t they love about spending money?

- How many different ways can you spend or receive money?

- What do they know about investment?

- How many of them experience financial anxiety?

The first 5–6 group discussions are the longest ones. From here, the definitions (as understood by your customers) come out. From these discussions, you will start seeing a pattern emerge.

You will discover:

- Definitions as per your customers (right or wrong)

- Pain Points

- What they love

- What they are oblivious about

- How they interact

- What technology they use

- What they would like (whether it relates to your line of business or not is a separate question)

- What they think you are offering

- What they consider the competition to be like

All these will form a basis for your question.

The best approach is to map the journey. Kanban is the best way to approach this mapping process.

It is extremely important that the journey map not be hidden away from the participants. It should be open for all to see so as to encourage further contribution.

Furthermore, for future sessions you can do A|B Testing by letting your group discussion members see / not-see the previous Kanban board and ask them to contribute.

It is a proven methodology, that the problem you seek and its solution literally comes out of group discussions using the kanban board method.

Assumptions reduce filters. In Physics, there is a concept known as:

Goldilocks Conditions: uses this concept to describe when the right conditions occur at precisely the right time to trigger a form of fundamental change.

The search for the Holy Grail for a Mobile Wallet solution is to find the Goldilocks Conditions that start an avalanche for traction and usage.

These are not theoretical concepts, but ones used by large and small companies worldwide.

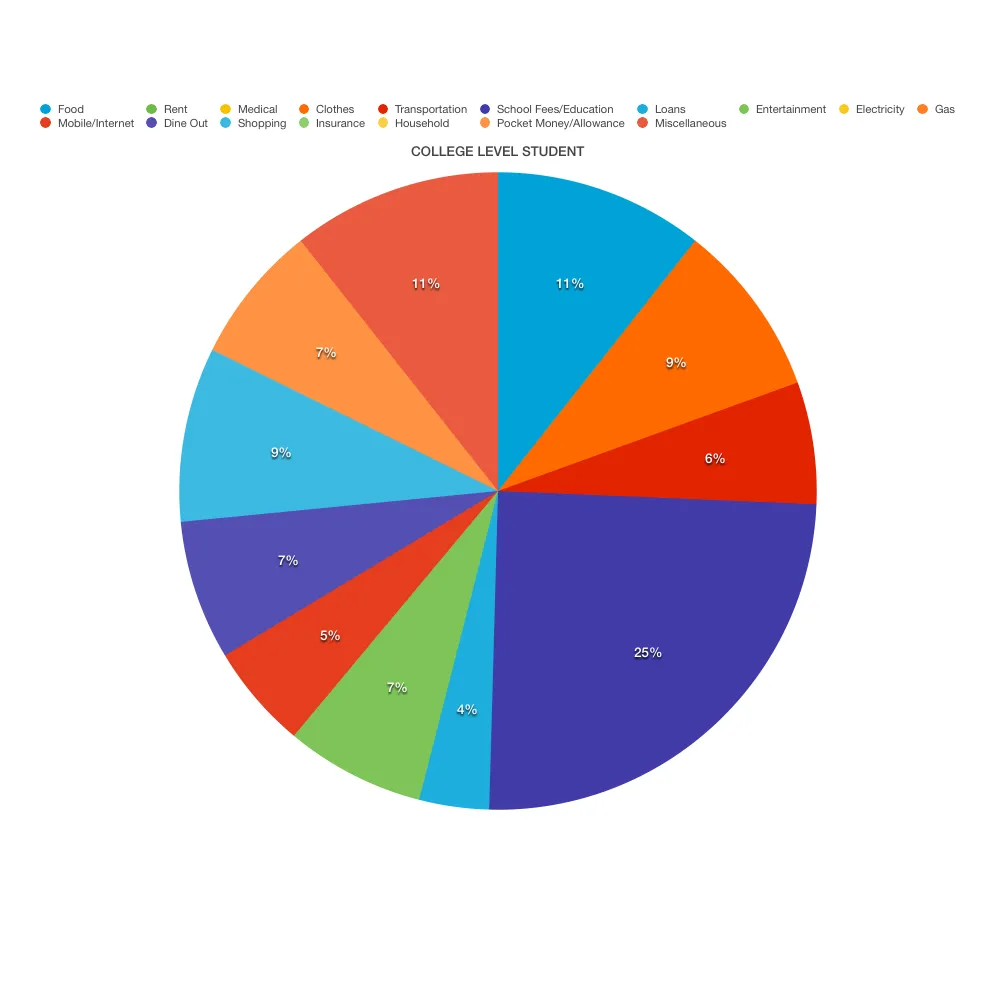

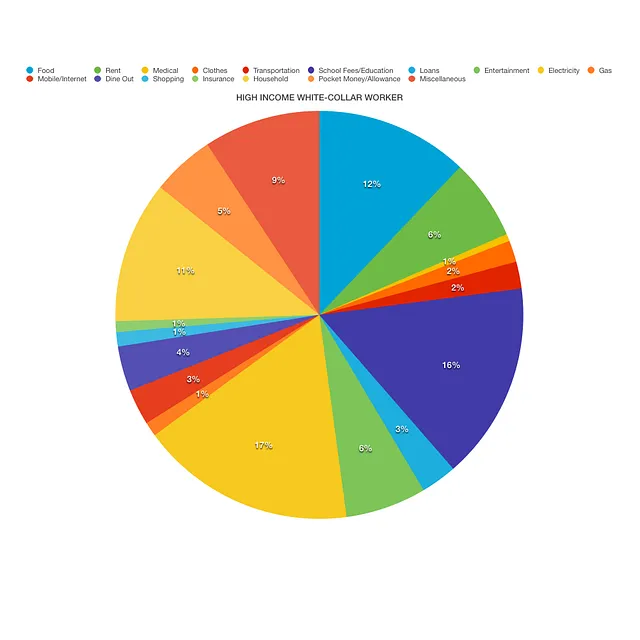

Personas: Who are my customers? What do I know about them?

Personas is one area many ignore. Why? Because it is a lot of drudgery. A painstaking process where you have to segregate profiles and work your way in thus creating individual personas of your customers.

Personas are the blueprints of any design solution. They answer the questions like Who, Why, What, Where, When, etc.

There are literally 10,000s of sources on the web, detailing how to go about building a persona (don’t forget to look at YouTube also).

Personas are templates. They serve as mini-resumes of your customers. You would never hire a person without looking at their resume, in the same analogy, you should never attempt to build a product/service without having the personas of your customers.

Some examples templates are shown below.

An argument against personas is that “our customers are different. they are illiterate, low-income and not educated”. Nothing could be further from the truth.

Everyone can have a persona. Everyone. Marry the spending patterns with the persona and you have very accurate portraits of your customers, along with their monetary tags.

The questions may be different, certain attributes may need to be changed and new attributes need to be added, but the gist of it should remain the same. You’ll give each customer an individual characteristic, from which your product development, marketing and sales teams can draw gold.

My Money vs. Your Money

How we shop and pay differs for each of us; the spending personas are a testament to that fact.

My earning / spending and monetary behavior is different from yours. Even after having such a unique spending fingerprint, personas can be grouped together in certain socio-economic classes.

Behavior is not a mechanical system but a human system – it is about people. Conformity is required, although it does force us to ask the same phrase/question, that is in life we all shop/spend differently. Finding the right sweet spot (grouping and customer classes) is not rocket science. It all boils down to an organization’s ability to model these classes in a single monetary operating system.

Perhaps a rhetorical question to ask — is there an equation that is all encompassing?

Sir Ken Robinson very eloquently put it in one of his TED Talks called: How to escape education’s death valley, which has a great message that can be applied here.

The point is education is not a mechanical system. It’s a human system. It’s about people, people who either do want to learn, or don’t want to learn…. So I think we have to embrace a different metaphor. We have to recognize that it’s a human system, and there are conditions under which people thrive, and conditions under which they don’t.

Every economic environment is a petri dish. It has to be observed, experimented with and with enough testing, you will get the formula right.

Digital Inclusion before Financial Inclusion

One moot point that many take for granted is the aspect of digital inclusion.

You cannot have financial inclusion without digital inclusion.

This is exactly why internet giants are spending $100s Millions on infrastructure, education and usability/stickiness methods to ensure that their future customers are onboard the digital inclusion bandwagon.

Not every wallet provider can provide a mechanism to include digital inclusion, but you certainly can act as catalysts for it. You can give your users a reason to take a step towards digital inclusion if you offer them something where they take the extra steps to come on board.

In Urdu (my native language), there is a word “Zaroorat” (literally translated it means “(the) need”). As long as you are able to package the need, their need, the customers will gravitate towards your platform/offering.

In simple words: Discovery of Necessity.

Some obvious, yet not so obvious things about money

Ben Milne, CEO of Dwolla wrote a brilliant piece on his blog regarding money (you can read the post below)

The take away point here is as follows:

If I have a $100 bill and I pass it to you, you now have a $100 bill. If you pass it back to me, I have a $100 bill. We can do this all day, and one of us will be holding on to a $100 bill.

Yet, if the same transaction is done electronically where say 3.0% + $0.30 is the fee, then the above exercise can only be done 79 times before the money disappears.

Think about it:

- Physical world (unlimited exchange).

- Digital world (79 times)

It is precisely this element (amongst other variables) that keeps the COD, Cash on Delivery, market alive in various developing world.

Why? Because there is no Cash-equivalent in the digital world. Or is there?

Solving the Cash On Delivery Dilemma

India, Pakistan, Mexico, Vietnam, Bangladesh, etc. are just a few examples of economies that are heavy on Cash-on-Delivery. When users purchase goods online, they prefer to pay cash upon delivery of goods. This is preferred by both the merchants — who don’t have to pay any merchant fees — and by customers.

What if transactions fees online went down to Zero? Yes, completely free. You now have the digital equivalent of cash (as far as spending/receiving of money is concerned).

Various surveys and studies have shown merchants will sign-up for services that have a zero-fees policy. It enables them to securely accept payments which in most cases are settled instantly.

In a survey conducted in India, Pakistan and Bangladesh of 200 medium to large sized merchants, who currently do not accept digital money, when asked if they would sign up for a zero-fee digital payment system, the results were as follows:

- Yes: 73%

- No: 3%

- Maybe: 19%

- Did not respond: 5%

No merchant likes to pay fees. If they can get around it, they will.

The model is not absurd, as many may title it. While there is no transaction money, the money is still being retained by the bank you partner with through a revenue-share agreement. Every bank’s core mission is to increase the number of account holders as well as increase the deposit volume.

The zero fees model addresses both these issues. In addition, value-led spending earns income for the wallet operator such as using your debit card at retail locations.

D/B/A: Doing Business As…

Another huge hurdle is the paperwork required for qualifying as a merchant. Many small to medium sized merchants are averse to signing up with banks &/or payment processors that require a long trail of documentation. Most merchants are unregistered and are doing business with their personal bank accounts.

DBA or Doing Business As is a methodology that can deflate this problem.

For example: Let’s say I have a business that sells mobile phones online. Let us assume my unregistered brand is simply a website or a board on my shop that says “BuyMobilePhones.com”

In the regular course of business, when people have to pay, they pay into my bank account, i.e. Faisal Khan. This not only looks unprofessional, but can be confusing at times.

If there was a method to sign up Faisal Khan with a DBA, then the merchant ID on record that would show up on receipts, etc. would be “BuyMobilePhones.com” rather than Faisal Khan.

Less confusion, less hassle and I always know by looking at my statement where the charge was made.

D/B/A is simply an alias.

We use it all the time in emails. info (AT) faisalkhan.com, for example, goes to my personal email address. Likewise, the same analogy can be used with individual and businesses.

We create an alias.

This is local to your system and hence it does not violate any existing law as it is because this DBA referencing is for your own internal use only (or rather that of your ecosystem).

A D/B/A can be thought of as a Customer ID. Rather than a number, it is a name.

Open-Wallet: Financial Routing & Aggregation

Open transaction platforms are built so as not to limit the number of ecosystems they can interface with. By utilizing APIs and connectivity to external payment systems (eg: VISA/MasterCard), et. al. one actually increases the value proposition of the wallet.

There is a large movement in designing payment systems that have access to aggregators and the ability to do financial transaction routing. This could mean, in the future, your wallet could be linked to PayPal, your bank account, Payoneer account, have a direct facing DDA access, remittance ID, etc.

The wallet divorces itself from the basic notion of being a stand-alone product and is much more than the wallet itself. It is a transaction hub.

One can clearly imagine the benefits of a money mobile wallet that is connected to other e-wallets/mobile-money wallets. Just think about it — being able to connect to a bKash wallet, an M-Pesa wallet, Easy Paisa wallet, Solid Trust Pay Wallet, PayPal wallet, etc.

Channels: Online / Offline

Wallet offering surveys done by various research led groups have studied ecosystem in Kenya, Philippines, India, Bangladesh, and Brazil (to name a few) and have found that a wallet must adhere to the omni-channel offering. Its usage should not be restricted to online or offline. It should have the ability to be used on traditional POS networks, online, in person, contactless payments and even QR based payment system.

The balance is always retained at the ledger-level, but the usage is not. Customers can use their wallet anywhere, Be it fee or free, with respect to spending their money.

The hybrid nature of fee or free cannot be disassociated from the over all characteristic of an omni-channel offering.

How a wallet ought to be rather than what it is forced to be

The wallet itself is a subject of much debate. Think of the physical wallet you may own. You can put any currency in it. You can put in pieces of paper (receipts?), photographs, your ID, loyalty cards, etc.

There is no condition that when you spend money, the wallet manufacturer will ask for a fee or every time you stuff currency notes into it, the wallet manufacturer says, oh 1.0% is mine!

Furthermore, there is no conditionality that you can spend your money here and not here. If this were the case, you’d never buy the wallet.

Yet, when we discuss mobile money wallets, all these absurd conditions are common and we are okay with it.

Think about that for a minute. Compare the freedom of your physical wallet to that of the digital wallet — the latter is much more restricting. It need not be this way. Read the article below which offers more insight on wallet freedom-vs-restriction on the physical-vs-digital wallet.

A mobile money wallet can be much more than just money. It can have coupons, bill payment, loyalty, ID verification, chat, social media connects, etc.

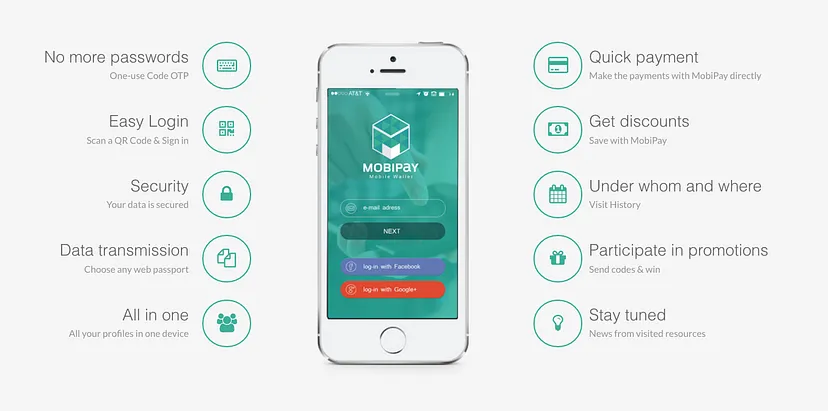

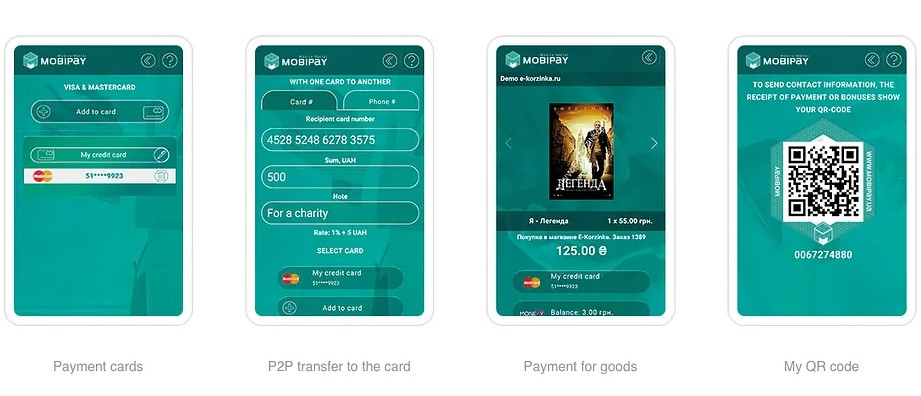

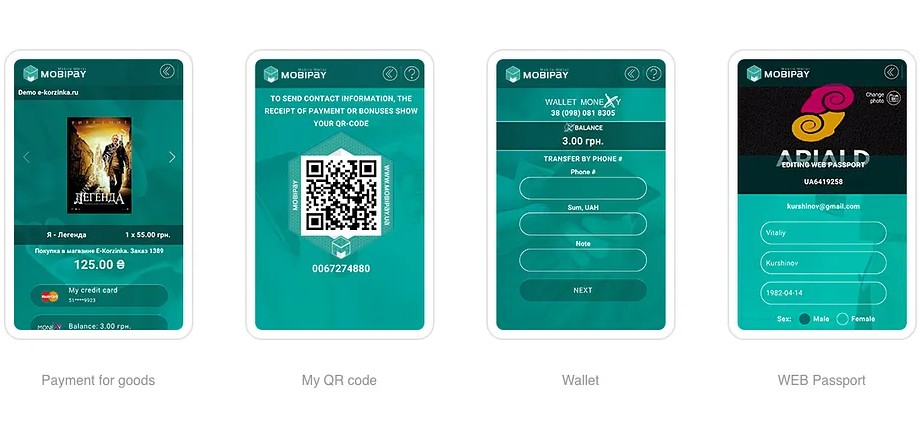

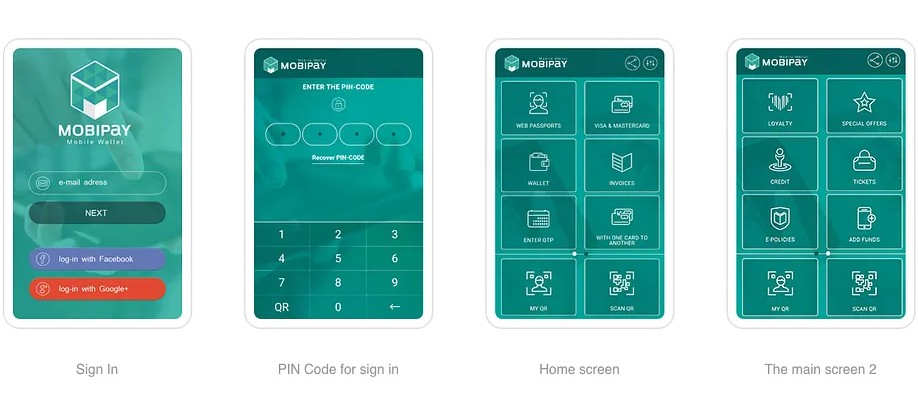

A company I came across recently, MobiPay is a great example. I have no affiliations with them, just happen to like the product.

MobiPay is one of the few examples (there are others as well) who are able to sell you not just the wallet, but the source-code as well.

The offering is quite extensive. They have both an IOS and Android version which can be downloaded and you can use the app in demo (or live) mode.

And if you love QR codes, well MobiPay has that too.

As I cited, I have zero affiliations with them, it would be worth while to check it out. I was thoroughly impressed by them. I can think of perhaps a dozen or so OEMs that also offer their source code, so dig deep, you never know what kind of bargains you can pick up.

Not everything you see needs to be present. Customization is the key here as per the data provided by your research and personas.

A huge question is whether to go with feature phone app, smartphone app or both. My (personal) opinion is that feature phones should be dropped altogether.

Concentrate on the smartphone. It’s where the future is. Smartphones also give you a much needed agnostic advantage over the telco carriers.

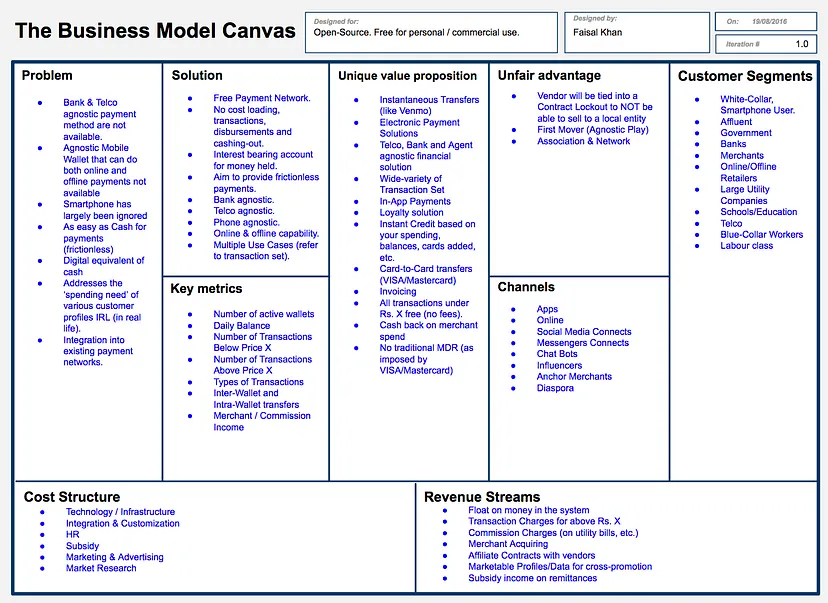

Lean Canvas: What would it look like?

To put the entire business case in a lean canvas template, please refer to the diagram below. The canvas can be downloaded from here.

Feel free to use the canvas, there are no copyrights on the canvas.

UI/UX

Commonly, the UI/UX is not given enough attention. Well-designed applications take feedback from literally 1,000s of users about what they like/dislike, how they interact with the app and what could be improved.

Steve Jobs exemplary command over design was legendary. He was so meticulous in his approach, that every pixel had to be justified. Every function, placement, etc. was examined and reexamined.

Proper UI/UX can offer an equal opportunity for right-handed users as well as left handed users. Short length fingers to long fingers, small fingerprint areas to large, regular sight to colorblind.

All is accounted for.

Industry veterans who excel in UI/UX design for the mobile, swear by the numbers. Field study samples of at least 5,000 customers is what provides a great feedback loop for improving design, form and function.

Engagement: Creating Stickiness

A well designed mobile money wallet is more than just payments. It is a marriage of curated content + transactions that enable an ecosystem to flourish.

Traditionally, we are programmed to view the wallet as a paying function. It can be much more than that. Curated content that is matched to individual spending profile of ever user can result in a great stickiness option. Look at the likes of what PFM (Personal Finance Manager) apps do, eg: Mint, or Moven does. These visual layers on top of the transaction data stream make the whole experience of visually looking at your money more appealing, whilst at the same time providing users with additional transactions options (i.e. up-sell/cross-sell) products and services to them.

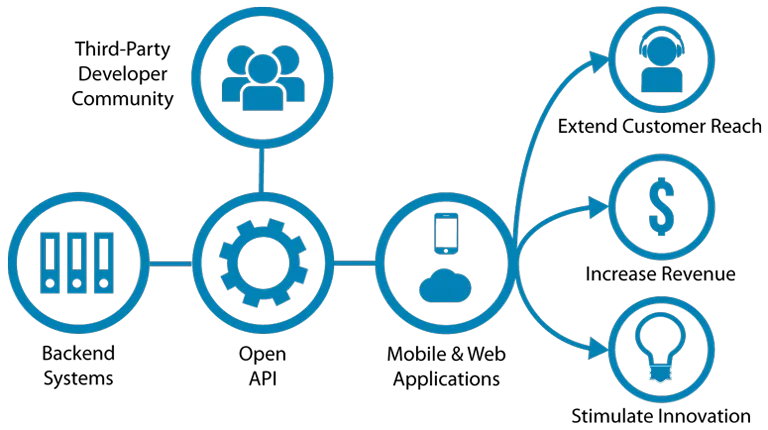

Open up your APIs

Innovation can come from various corners. One sure shot of increasing innovation on your own product, is to open it for others to develop apps for it. Open APIs is a great mechanism by which it can act as a catalyst to stimulate growth in an otherwise stagnant industry.

Research by various OEMs reflects this theory. Wallet provider who opened up their APIs experienced great brand loyalty, service offering and more revenue per user (when normalized) than with those mobile money operators who did not.

Many business opportunities are local to an economy and are often overlooked or missed by the OEMs. This is where APIs can make a huge difference. People will tinker with their ideas and entrepreneurs will look this as a floodgate of opportunity and cash-in on it. Most will not be successful, but those that genuinely address a problem and are able to provide a solution to it, using the APIs, will do well.

The Merchant Base

“Build it and they will come.”

This is an old-age saying that is very pertinent today. To digress a bit, in the mid 1990s when Motorola was rolling out the Iridium satellite phone program, the CEO of Motorola called upon his team.

He tasked them to visit every country in the world and sign-up with every telecommunications carrier.

I’m paraphrasing here, but a question was asked, “What success rate should we be looking at?” The answer was: “100%, we cannot risk that a client to be on the field with our phone, only to find out that the one carrier we did not connect to, is the one they needed to connect!”

Over the next 3 years, Motorola’s sales team did just that. Each and every market where Motorola was allowed to do business (as per US Government regulations) was signed up. Each and every.

It is hard work, but someone has to do it.

The same needs to be applied to the merchant base in your economic activity zone. Its about probability. With the spending personas data you have, you will have a detailed list of all the merchants your customers use. Then it is your sales force that has to go into the field and sign them up.

The probability of a customer going out and their wallet to pay at any given merchant needs to be high. Quite high.

When the number of merchants…

Who accept wallet payments> those who do not

Consumer confidence in wallet usage gets a boost.

For any given launch of a wallet service, it is imperative that the merchant base be secure, i.e. they have signed up. It gives a user no confidence to walk into an establishment only to find out that the merchant does not accept your wallet payment method.

The wrong notion is to build a customer base to force the merchants to sign up. That’s akin to asking hungry customers to walk into a restaurant, only for the restaurant to say, sorry, we’re not operational or we don’t serve that particular type of dish. Only when we will see a demand for that dish, would be perhaps change out mind. It just doesn’t work that way.

Merchant sign-ups before customer walks-ins is a prerequisite.

Not the end of cash

A digital wallet is not the end of cash. Though many would like it, unfortunately, in many, many developing economies, for various reasons, cash remains king and it would not be disappearing soon. At least not at the rate pundits are predicting. At present it makes sense to have payment systems that can co-exist together with the cash economy.

A hybrid co-existence of digital and analogue cannot be emphasized enough. Both ecosystems are here for the next couple of years, with the cash society slowly losing ground to the digital society.

A well-designed mobile money wallet solution will take this into consideration and interface with cash based transactions.

Conclusion

The points listed in this article are by no means complete. Any large scale deployment of a mobile money wallet is continually evolving. A great example if that of PayPal (albeit distributed). Whilst PayPal’s core remains the same, P2P, they have ventured into other areas such as remittances, bill-payments, retails, social payments, etc. Eventually, all these product variations will be offered under a single umbrella of the main PayPal product as well as continue to maintain the standalone status (of Venmo, Xoom, etc.)

—

This page was last updated on January 13, 2025.

–