What Exactly Is “Remittance-As-A-Service” ?

Remittance-As-A-Service (or RaaS for short), is a turn-key solution that provides:

- Access to the US (domestic & international) peer-to-peer money transfer market

- Legal cover for Money Transmitter Licenses

- Banking arrangements*

- FBO (For Benefit Of) Pooled Accounts

- On-Boarding (CIP/KYC)

- AML/CTF, etc.

- Payment Processing*

- Access to Payment Networks & Settlement

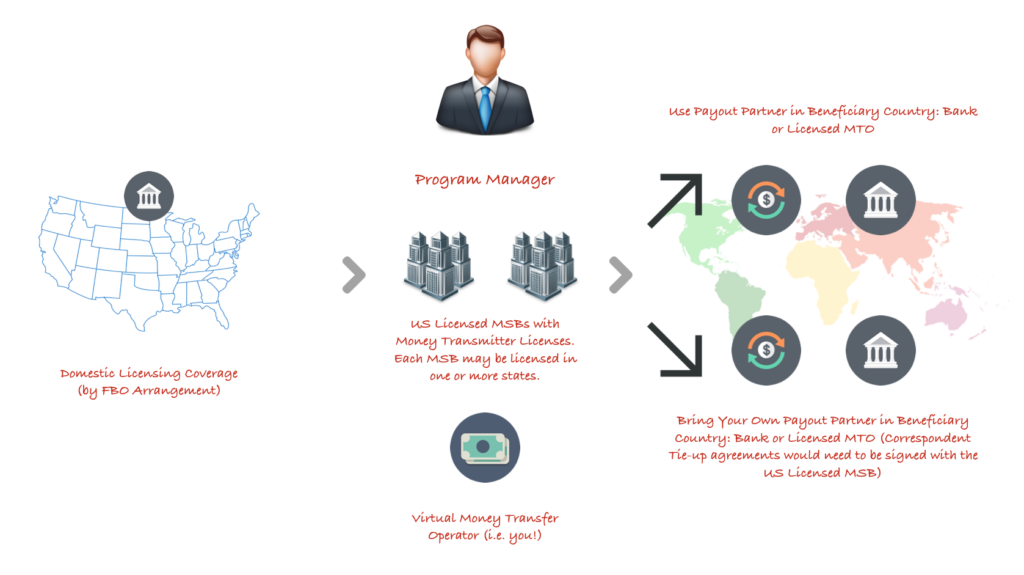

- Access to Beneficiary Country Banks/MTOs

- Option to BYOBB/BYOMTO (Bring-Your-Own Beneficiary Bank / Bring Your Own MTO)

- FX Handling (Optional)

- Infrastructure (Web/API), etc.

Who Runs This Service?

The RaaS offering is provided by what we call a Program Manager. The PM (which is a company) is responsible for integrating (legally, technically, etc.) with all parties, to offer a Single Contract for the vMTO (virtual Money Transfer Operator) to sign and begin work.

You will sign the contract with the Program Manager.

The Program Manager is not a licensed entity. The contract you sign with the PM provides the legal and dotted lines with the licensed entities that provide you coverage.

This has been cleared by lawyers and a legal opinion is with us. It is also accepted by the State Regulators and the legal counsel of the license holders.

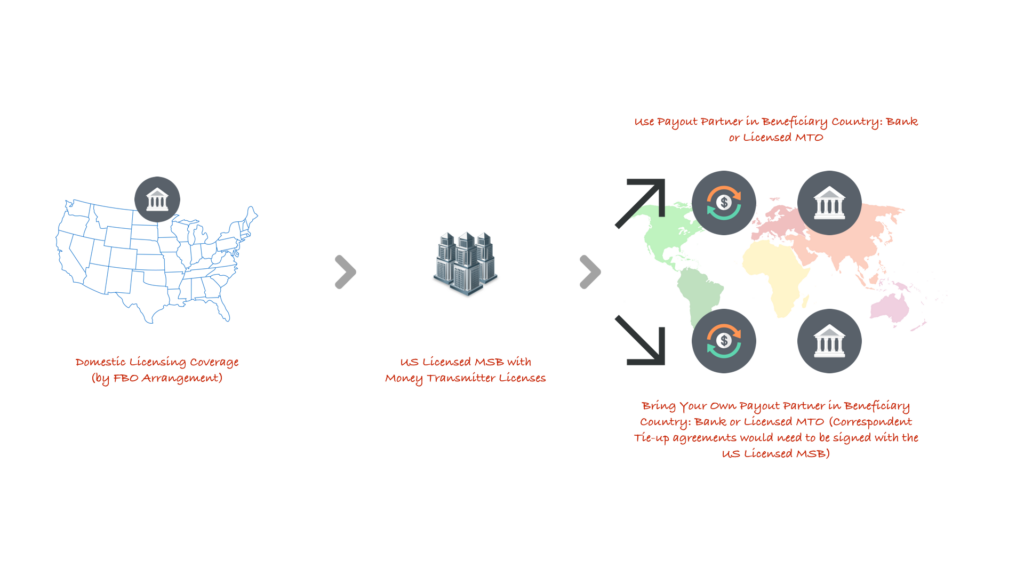

Ecosystem Layout

Here is a top view of how the ecosystem of the RaaS offering looks like:

What Does Licensing Entail?

There are TWO licensing aspects to the RaaS:

- Domestic Transactions (50 US States), provided as an FBO (For Benefit Of) account.

- International Transactions (24 US States are covered so far by various MSBs)

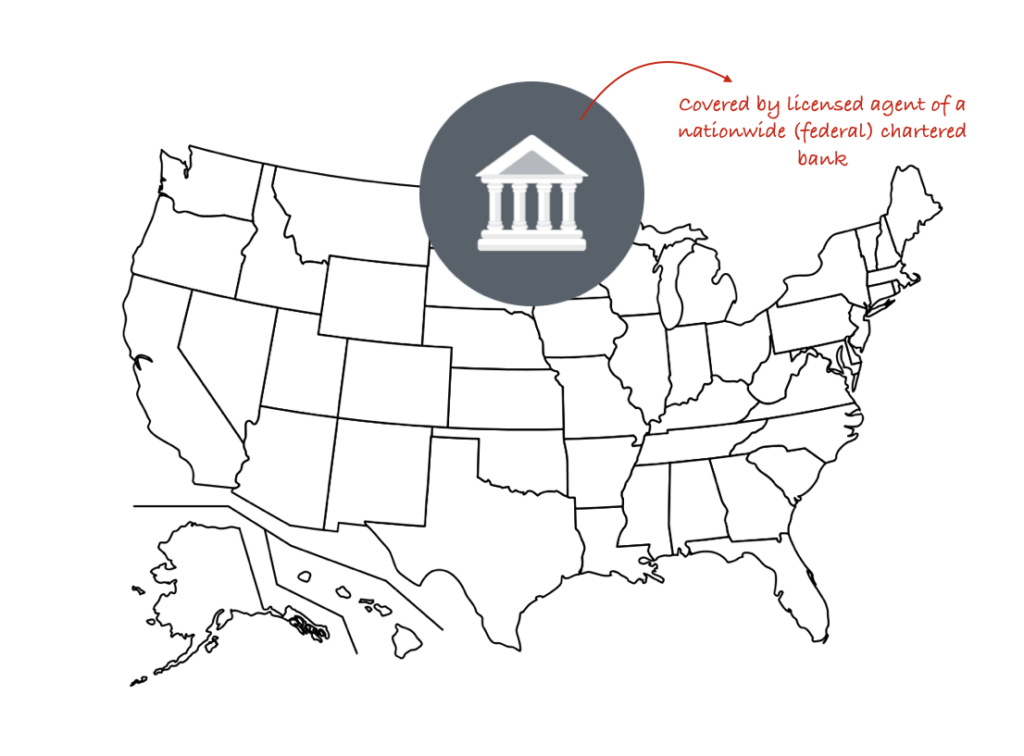

Licensing (Domestic Transaction) – 50 US States

On the domestic licensing, i.e. for peer-to-peer transactions between customers of all 50 US States, we have a Banking Agent who provides FBO (Pooled) Accounts.

Customers from any of the 50 States can sign-up, under your brand. Your TOS will clearly mention that the customer is opening an account with the Banking Agent (who is providing the FBO arrangement).

The funds are with a licensed bank with a nationwide charter. The banking agent provides instructions on funds handling on your behalf, which the bank then executes.

The instructions to the banking agent are provided via the API.

At no point in time do you (the vMTO) touch the funds. The funds’ liability is undertaken by the bank itself. The bank will only cover US transactions.

Licensing: International Transactions

To be given coverage for international transactions, the following must be understood first:

- When funds exit from the pooled account to go overseas, a licensed entity must be responsible for the liability and delivery of the funds (as the bank’s coverage has ceased at this point in time). This is extremely crucial.

- Here, we work with licensed MSBs who then take ownership of the funds from the pooled account (and associated liability) for onward settlement.

- Funds are released only to the associated Bank/MTO in the beneficiary country when they have released money to the end beneficiary and confirmed delivery of transactions.

- vMTOs must enter into a prefunded model with their respective Bank/MTO.

We have licensed MSBs who are covering the following States (including the big three):

Alabama, California, Connecticut, Florida, Georgia, Hawaii, Illinois, Maryland, Massachusetts, Montana, Michigan, New Jersey, New Mexico, New York, North Carolina, Nevada, Oregon, Pennsylvania, Rhode Island, South Carolina, Texas, Utah, Virginia, Washington, Louisiana, Montana, New Mexico.

As more MSBs on-board with us, not only do we increase the number of States, but we also offer resilience on the coverage (especially for the big three states).

We expect to have full 50 State (redundant) coverage towards Q3 2016.

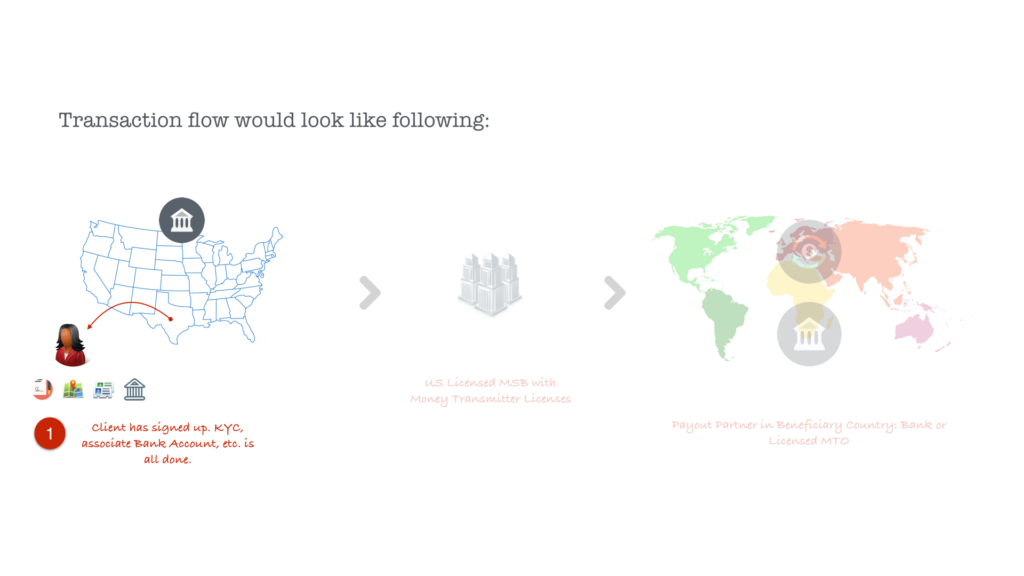

Domestic Licensing: Flow of Funds

The section below describes the various stages of the flow of funds for how domestic (US only) customers are signed up and how they will be dealt and covered.

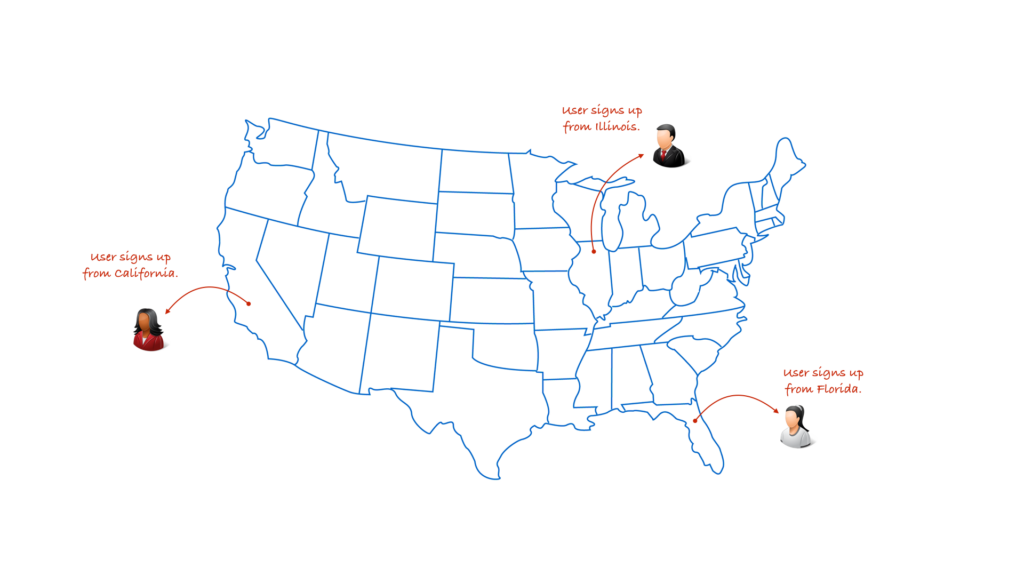

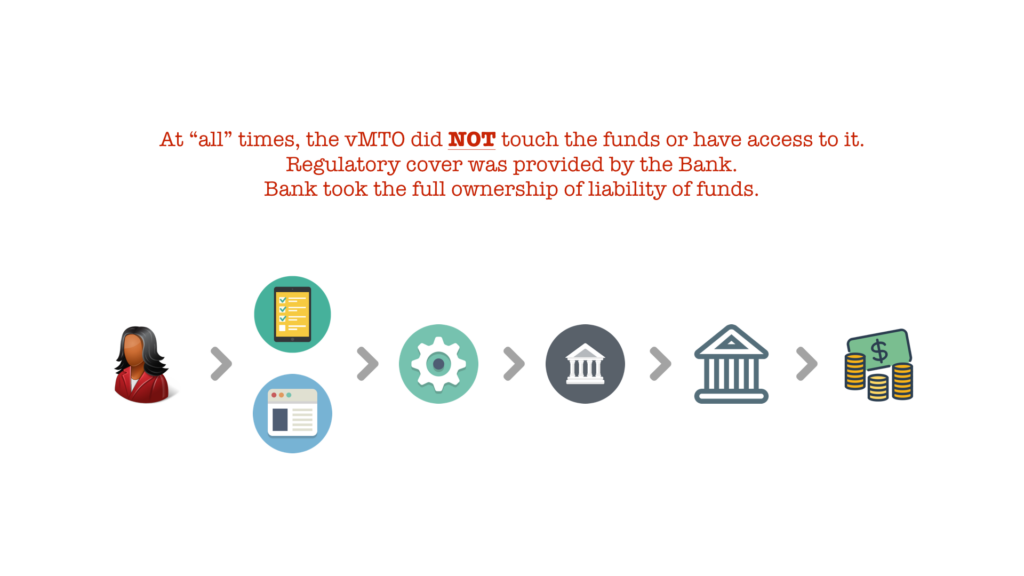

Domestic Licensing: How Does it Work: Step 1: Users from various States sign up.

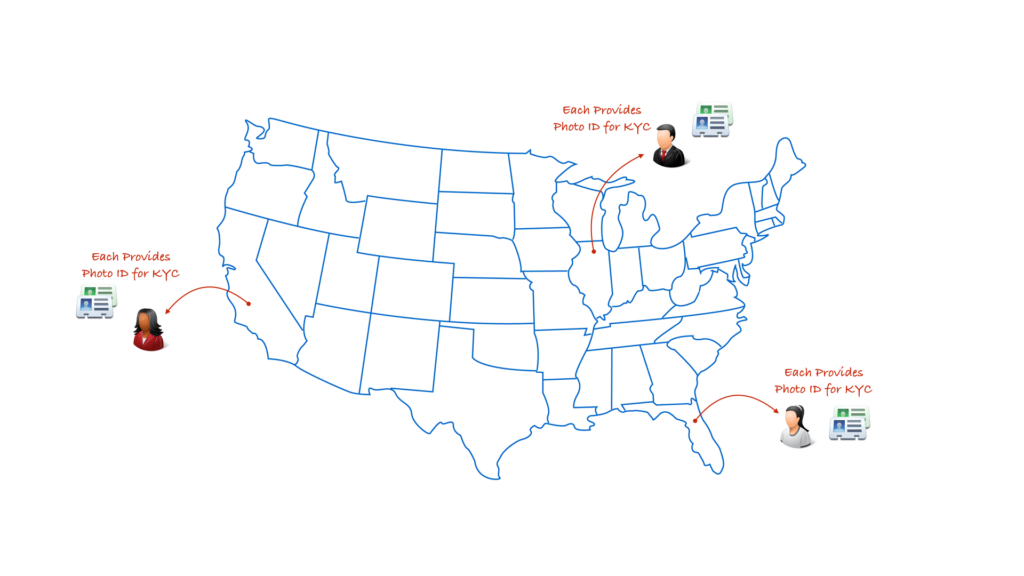

Domestic Licensing: How Does it Work: Step 2: Users provide Photo ID scan/information for purposes of KYC.

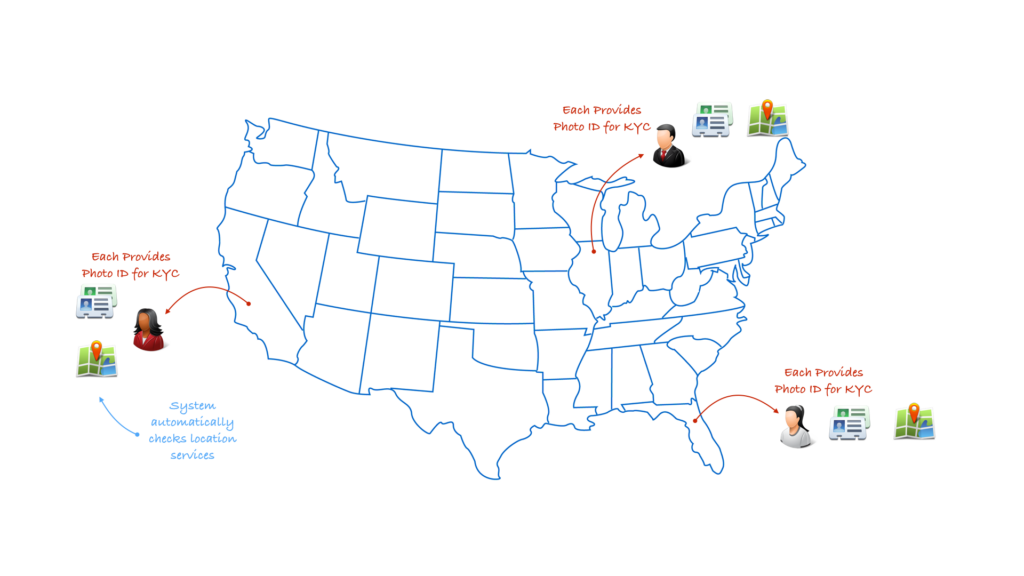

Domestic Licensing: How Does it Work: Step 3: System checks for various attributes as to where you are logging in from, what is the address / mailing address information provided upon registration and for which state you are a resident of.

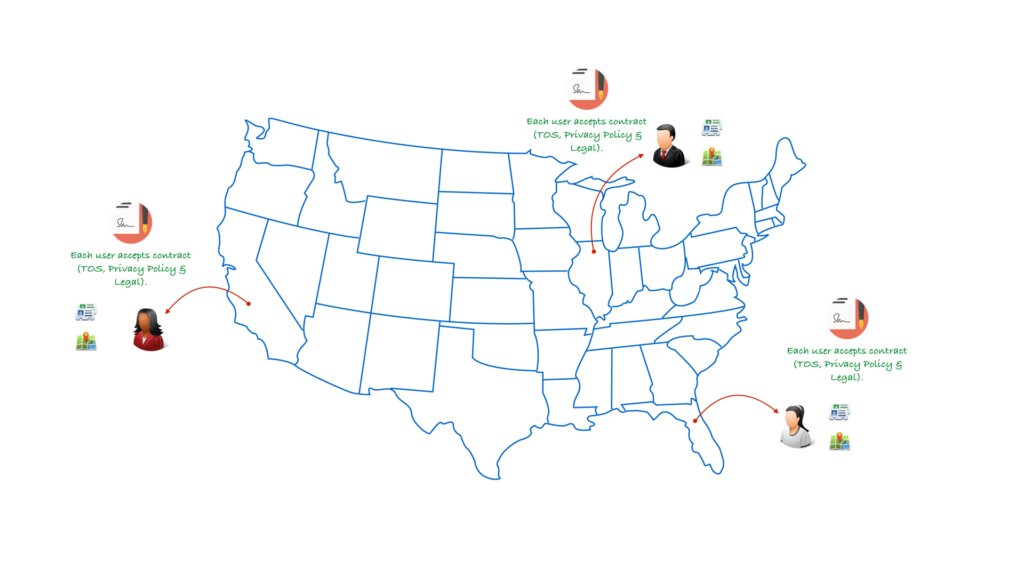

Domestic Licensing: How Does it Work: Step 4: Users agree and accept to the Legal/Terms of Service.

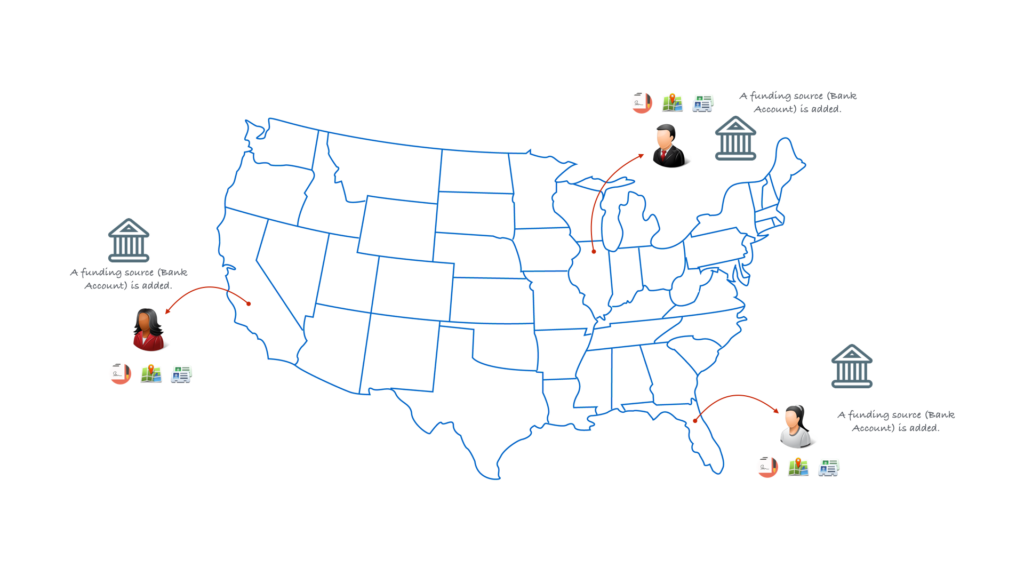

Domestic Licensing: How Does it Work: Step 5: A funding source like a Bank Account must be attached to your account.

Domestic Licensing: How Does it Work: Step 6: After adding the funding source, money can now be loaded into your account/wallet.

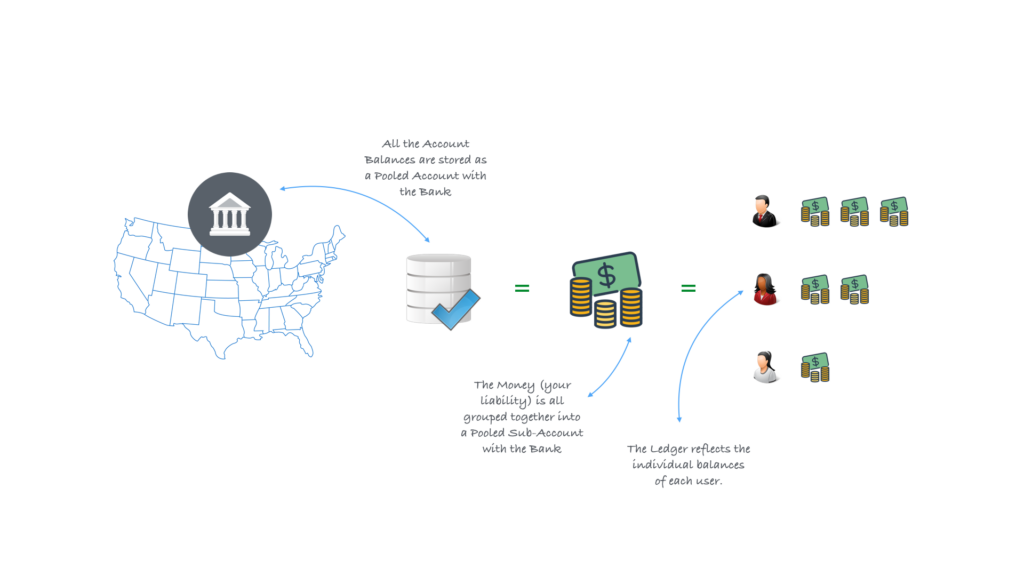

Domestic Licensing: How Does it Work: Step 7: All the Account Balances are stored as a Pooled Account with the Bank. The Money (your liability) is all grouped together into a Pooled Sub-Account with the Bank. The Ledger reflects the individual balances of each user.

Domestic Licensing: How Does it Work: Step 8: For transfers: Users interact with the app (provided by the vMTO or the Program Manager). The App sends the API instruction to the Banking Agent, who in turn sends these instructions to the bank, which executes the instructions.

Domestic Licensing: How Does it Work: Step 9: At “all” times, the vMTO did NOT touch the funds or have access to it. Regulatory cover was provided by the Bank. Bank took the full ownership of liability of funds.

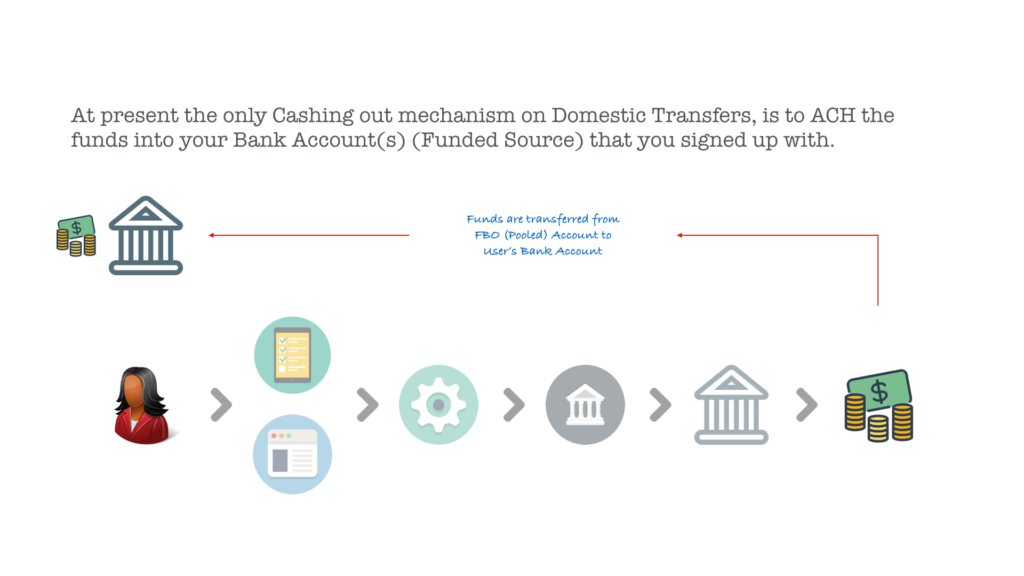

Domestic Licensing: How Does it Work: Step 10: At present the only Cashing out mechanism on Domestic Transfers, is to ACH the funds into your Bank Account(s) (Funded Source) that you signed up with.

International Licensing Coverage & Transaction Flow

International transactions coverage flow of funds and process is described below.

International Licensing: How Does it Work: Step 1: The three parties in the international transaction are: The Domestic Bank, the Licensed US MSB and the Payout Bank/MTO in the Beneficiary Country.

International Licensing: How Does it Work: Step 2: You can use an existing payout partner relation that the US MSB has in the beneficiary country or you can bring your own payout partner where payments need to be made. You are also allowed to use any other licensed payout partner for purposes of treasury services.

International Licensing: How Does it Work: Step 3: Client has already signed-up, done the KYC, added a funding source, and loaded their wallet.

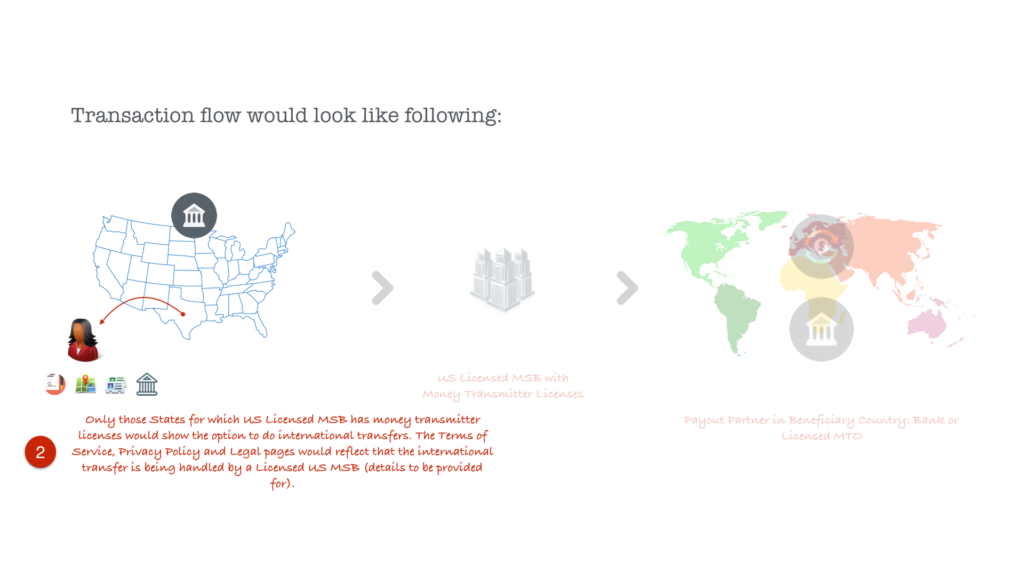

International Licensing: How Does it Work: Step 4: International Transfers would only be shown for states in which the US MSB is licensed in and holding valid money transmitter licenses.

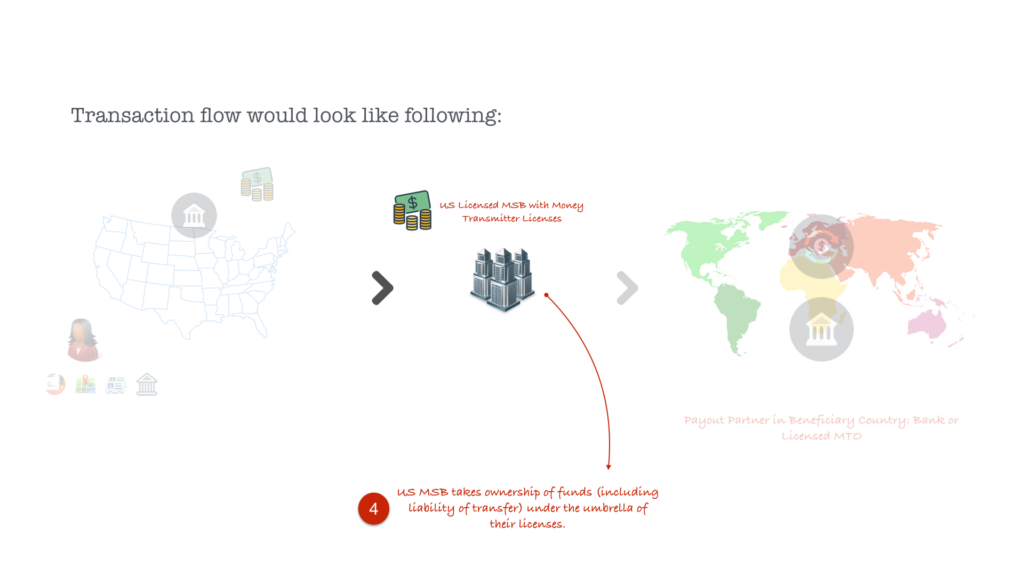

International Licensing: How Does it Work: Step 5: Money that needs to be transferred overseas, gets deducted from the User’s Account (Wallet) and gets moved into the Pooled Account.

International Licensing: How Does it Work: Step 6: The money is then transferred from the Bank’s Pooled Account into MSB’s Pooled Account, hence the MSB has now taken over full liability on the transfer of funds.

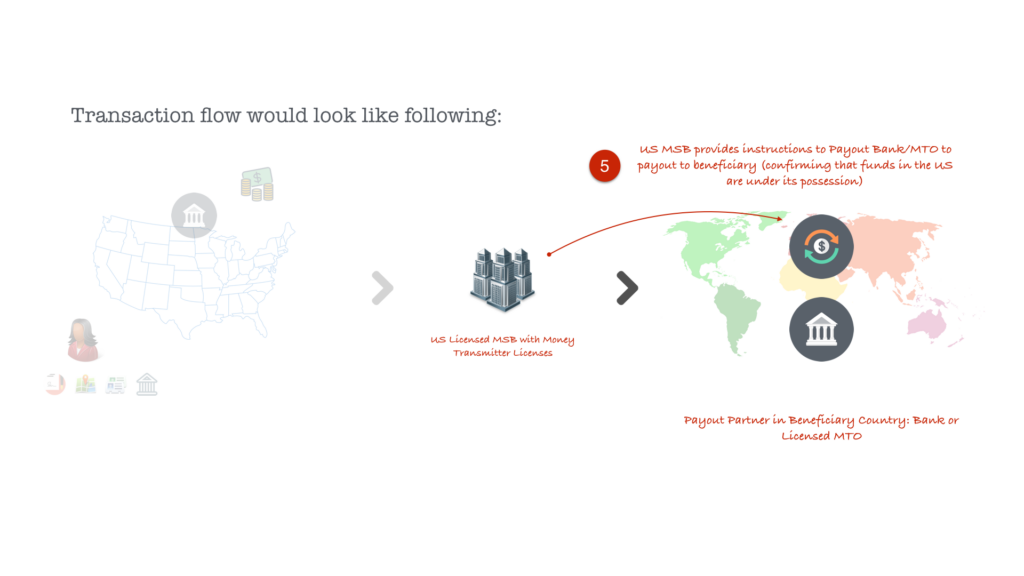

International Licensing: How Does it Work: Step 7: Once the funds are in possession of the US MSB, they then (via an API call), let the vMTO / Payout Bank know that funds are in their possession, and that the Payout Partner should pay the money to the Beneficiary from their Pre-funded account.

International Licensing: How Does it Work: Step 8: Payout Partner pays out the money to the beneficiary.

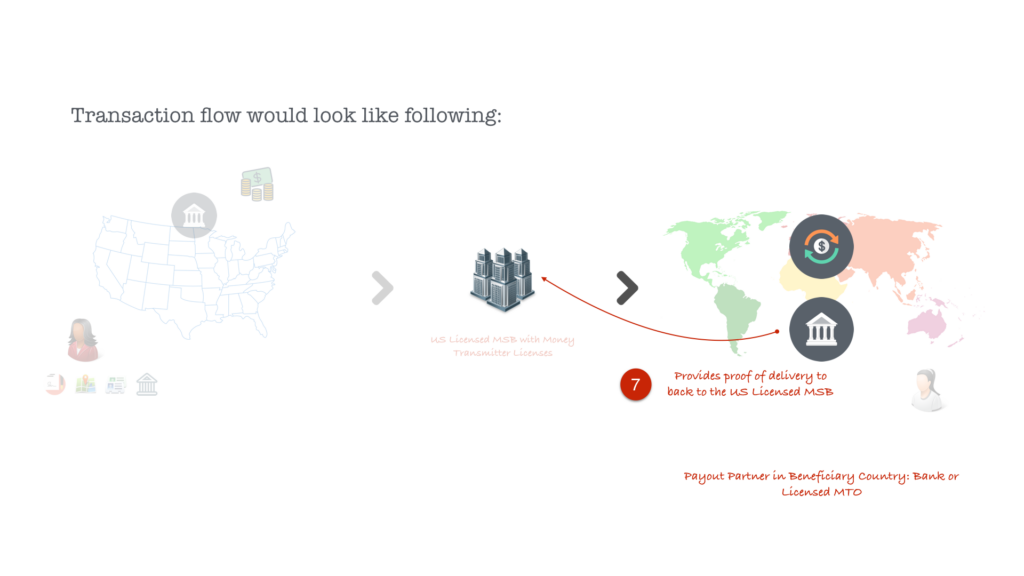

International Licensing: How Does it Work: Step 9: The Payout Partner then (via an API call) informs the US MSB that payment to beneficiary has been completed and proof of delivery (electronic) is provided to the US MSB.

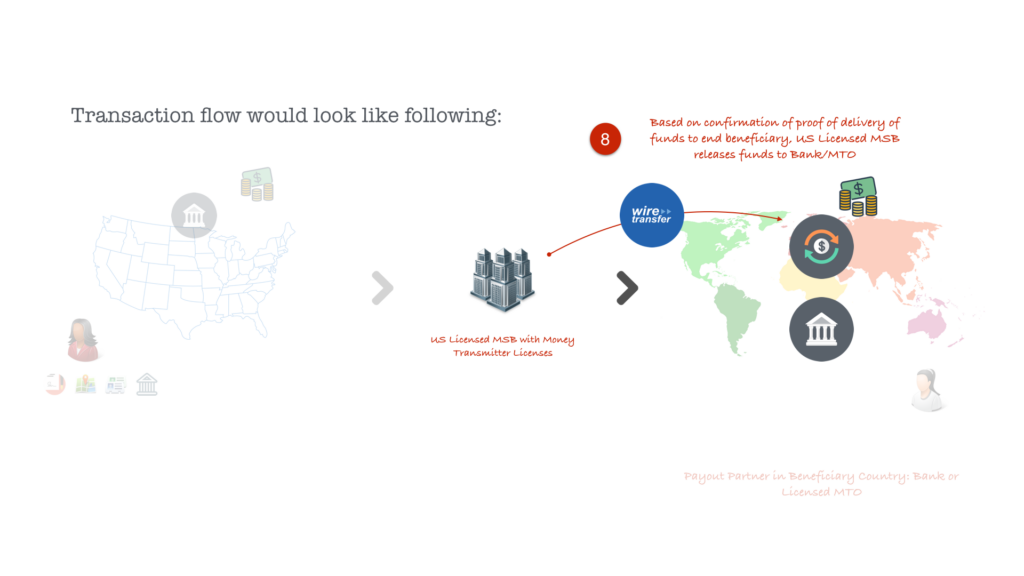

International Licensing: How Does it Work: Step 10: Once the Proof of Delivery of Funds have been received, the US MSB wire transfers the funds to the payout partner bank/MTO as per the agreed contract.

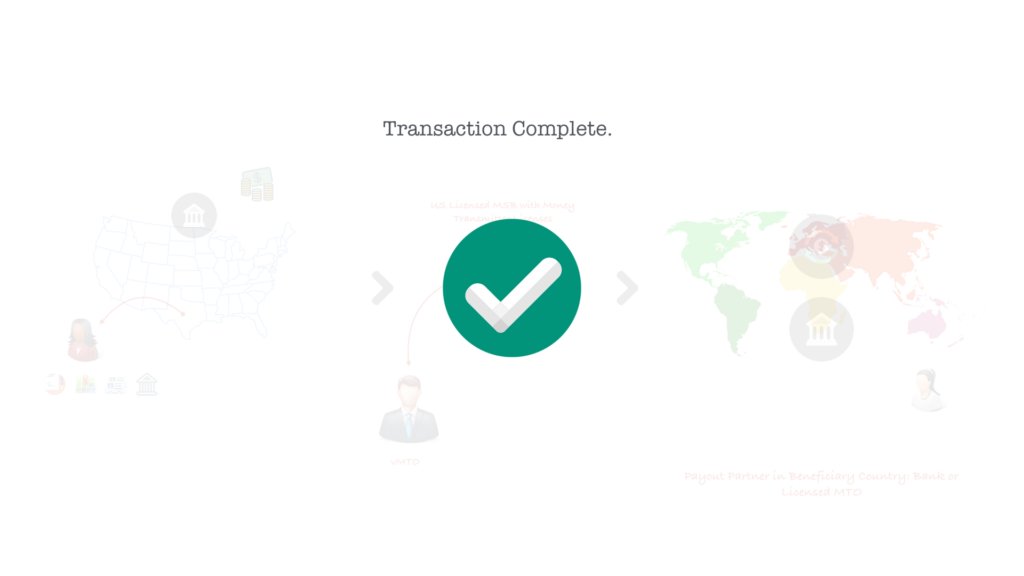

International Licensing: How Does it Work: Step 11: The commissions for the vMTO are then pushed into their designated account as per the agreed contract.

International Licensing: How Does it Work: Step 12: This essentially completes the transaction and completes the liability cycle of all parties involved.

What Options are available to Clients?

Remittance-As-A-Service (or RaaS for short), comes in a variety of options, as listed below:

Using Our Web Platform

- Option 1: We Provide Web Platform + Delivery of Funds in Beneficiary Country.

- Option 2: We Provide Web Platform, You provide Delivery of Funds in Beneficiary Country*.

Using Your Own Platform

- Option 3: We provide API + Delivery of Funds in Beneficiary Country, You provide Product Build.

- Option 4: We provide API, You provide Delivery of Funds in Beneficiary Country* + Product Build.

API App Usage

API App development usage, has to be cleared with the MSBs before it can formally be launched. Such approvals would include:

- Flow of Funds (understanding)

- Intent Template (what is the intent and transaction set of the application)

- Detailed breakdown of the transaction set

- Technical understanding: e.g.number of API calls, hosted platform, etc.

- Notification and transactions receipts format & text.

- Reporting

- Etc.

Who is responsible for KYC?

The CIP (Customer Identification Program) is set by the Bank and the MSBs. You would have to meet (or exceed) the requirements.

The Bank & MSBs have their own on-boarding process for KYC which cannot be by-passed. You would have to use this system and on-board your clients.

Any external system you employ for KYC, etc. is for your benefit only and cannot be substituted with what the Bank & MSBs have in place.

A photo ID is mandatory for opening an account in the US.

Who is responsible for AML, Screening & Reporting?

The Bank & the MSBs are responsible for it.

On the beneficiary side, the licensed entities (either a Bank or an MTO) would be responsible for it.

Applicable Terms & Conditions

- Acceptable Payment Methods

- Application Assessment Fee

- Due Diligence Documents Requirement

- How Do We Charge Our Fees For Commercial Service?

- How To Submit a Detailed Flow-of-Funds (FoF)?

- List of Restricted or Sanctioned Countries

- Personal KYC Information

- Prohibited Products & Services List

- Referral Agreement (Sample Copy)

- Remittance as a Service (RaaS) Pricing

- Refund Policy

- Terms & Conditions

- What Financial Institutions will Charge You for USA Regulatory Coverage

- Why we do not sign an NDA (Non-Disclosure Agreement)

Prices & specifications subject to change without notice.

—

This page was last updated on November 23, 2022.

–